Procter & Gamble Company (PG ) is a leading household and personal care manufacturer that has been around since 1837. Now the company is more known for its famous brands like Gillette, Cascade, Bounty, Crest, Oral-B, Febreze, Tampax, and Old Spice. The company markets its products globally, through merchandise stores, grocery stores and drug stores.

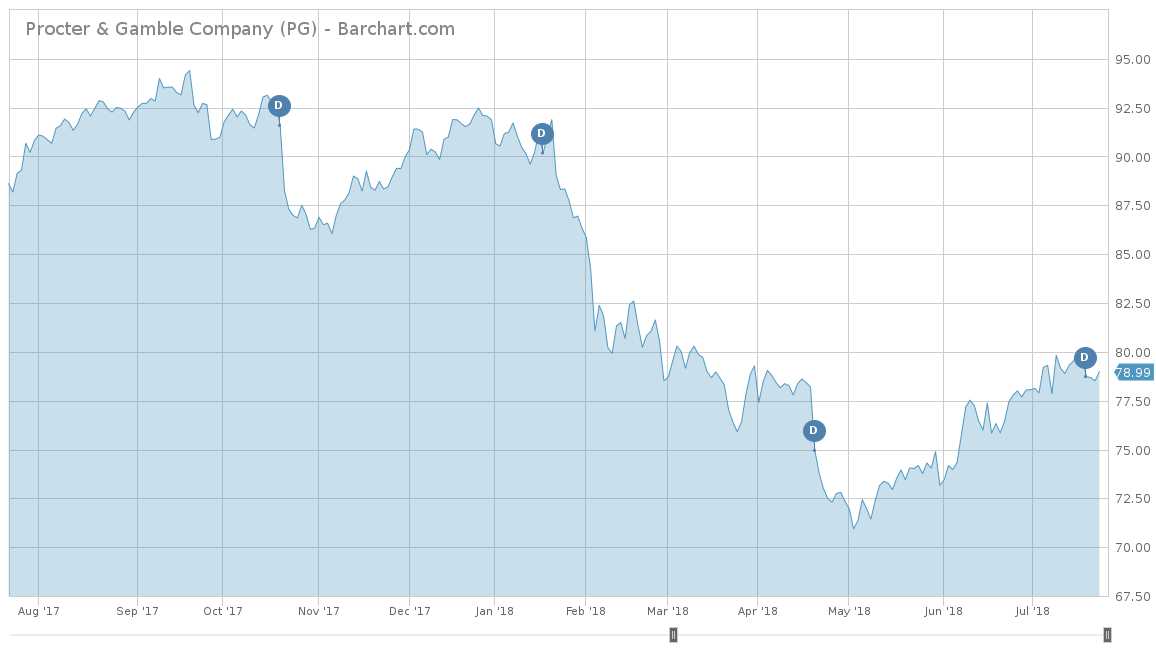

On a year-to-date basis, Procter & Gamble has had a terrible start and is down 14.03%. This holds true for both the one-year and five-year trailing returns, which are also down 10.42% and 1.59%, respectively. Compared to the S&P 500, PG has underperformed in all three time frames. On a year-to-date basis, the S&P is up 5.49%. Same goes for the S&P 500 over the longer term, as the S&P 500 has returned 14.19% for the trailing one year and 67.29% for the trailing five years. Unilever PLC (UL ), although considerably smaller by market cap, is a major competitor of Procter & Gamble. Unilever also outperformed P&G in all three time frames, with returns of 1.84%, -0.25% and 35.51%.

Fundamentals

Over the last five years, P&G has had a negative 4.5% average for its revenues, with its last positive growth happening in 2013. Most recently though, P&G had a successful third quarter (their fiscal year is from September to June) with revenues of $16.28 billion, up 4.3% on a year-over-year basis. With one quarter remaining, analysts expect P&G to end the year with a total of $66.84 billion in revenues, equal to a 2.7% increase. This is mostly attributed to strong sales in its beauty, fabric and home care businesses. P&G has analysts convinced that their losing ways are behind them, with expectations of $67.57 billion in 2019, equal to an increase of 1.09%.

On an earnings-per-share basis, Procter & Gamble actually has had decent results with an average growth rate of 3.8% over the last 5 years. In fact, its only negative earnings year was in 2015 due to a decline in foreign exchange rates and a $2.1 billion charge as P&G changed its method for accounting for Venezuelan operations. For 2018, P&G looks to see another drop-off again mostly due to the second quarter’s EPS of $0.93 per share, a drop of 68% from the year prior. This is due to the Beauty Brands divestiture gain in the base period and a current period net income tax charge related to the recently enacted U.S. Tax Cuts and Jobs Act. For the entirety of 2018, analysts see P&G finally see earnings of $4.20 per share, a decline of 28.39%. Luckily, they also believe the drop-off was a one-time deal, with 2019 earnings estimated to be 7.86% higher at $4.54 per share.

Strengths

Procter & Gamble has made a conscious effort to become a leaner, more efficient company, as evidenced by the company cutting its number of brands from over 170 to 65. The company has also drastically reduced its product categories from 17 to 10, divesting non-profitable areas and focusing on the products that generate the higher sales margins. As such, P&G has 21 brands that currently each generate anywhere from $1 to $10 billion in sales annually. The next 11 brands generate $500 million to $1 billion in sales. Its crowning jewels are the fabric and home care categories and the baby, feminine and family care categories.

With such major labels and consumers who are still very brand loyal when it comes to the goods that P&G offers, expect revenues to stay on a steady upward trend.

Growth Catalyst

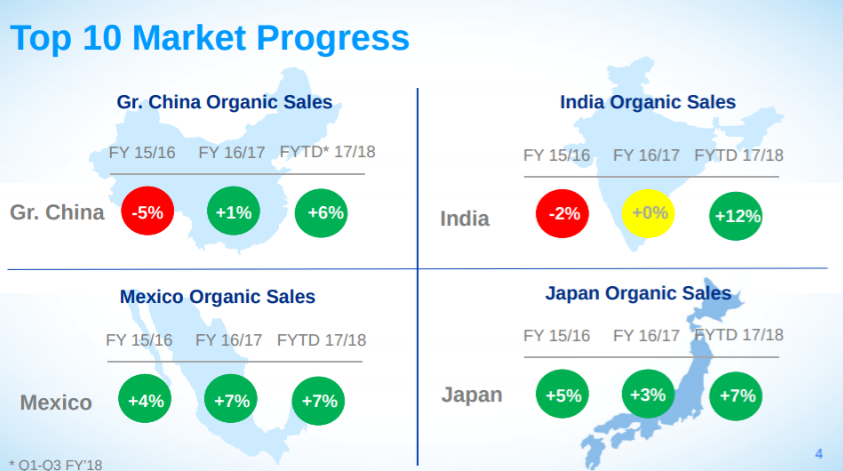

The biggest growth for P&G would be from its international presence, especially in China, India, Mexico and Japan. In terms of its 2017 year-end sales, P&G generates 55% of its revenues outside the U.S., Europe accounts for 23%, Asia Pacific for 9% and China for 8%. In the last year, P&G has seen 6% growth in China, 7% in Mexico, 12% in India and 7% in Japan. With this steady growth and P&G already holding market share in many of its products in the U.S., the future is looking very bright.

Dividend Analysis

Procter and Gamble has been one of the longest-running companies that has consistently raised their dividend. P&G has raised its dividend every year since 1957, over 61 years in a row. The stock has a decently sized dividend payout of $2.87 per share, equal to 3.58%. This is considerably higher than the average yield of the consumer goods sector dividend stocks, which is currently 1.76%. P&G’s dividend is also higher than Unilever’s dividend, which is currently yielding 3.20%.

Procter & Gamble is on the list of dividend stocks that have been increasing their dividends at least once per year for at least the past 25 years. Click here to see the list.

To find more high-quality dividend stocks, check out our Dividend Screener. You can even screen stocks with DARS ratings above a certain threshold.

Risks

The biggest risk to P&G would be declines in foreign exchange rates. With most of its business overseas, P&G will be held captive to the ever-changing exchange rates. This was perfectly evidenced in 2015, when P&G saw a earnings drop of 39%.

The Bottom Line

Despite a terrible track record over the last five years for its stock price, the future for Procter & Gamble must surely be brighter. However, earnings are expected to drop off in 2018, which was the primary cause of the double-digit stock price decline on a year-to-date basis. With the stock beaten down, now might be the time to buy if your portfolio doesn’t already own this blue chip stock. Do not expect high-flying returns by any means, just buy P&G as a slow, steady-growing company that consistently raises its dividend.

Check out our Best Dividend Stocks page by going Premium for free.