The industrial sector is highly cyclical, because these companies are heavily exposed to the global economic climate. This is why industrial firms are typically viewed as bellwethers for the broader economy. They have operations all over the world and serve a wide range of industries. As a result, the industrial stocks can be prone to higher levels of volatility. This makes it difficult for industrial companies to produce modest, steady growth from year to year.

However, Dover Corporation (DOV ) is a rare example of an industrial company that has generated consistent growth and paid reliable dividends for decades on end without interruption.

This consistency has allowed Dover to reward its shareholders with rock-solid dividends for many years. On Aug. 5, the company announced a 5% dividend increase. The new quarterly dividend rate will be $0.44 per share, up from $0.42 per share, and will be paid Sep. 16, to shareholders of record on Aug. 31. This is the 61st consecutive year in which Dover has increased its dividend, which gives it the third-longest streak of uninterrupted annual dividend growth of all listed companies, according to Mergent’s Dividend Achievers.

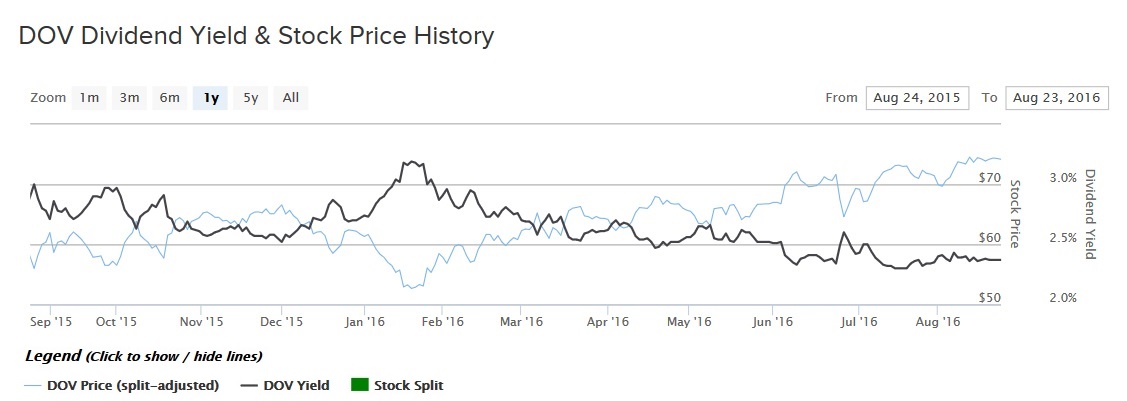

Dover stock has performed very well over the past one year. Based on its Aug. 23 closing price of $74.61 per share, the stock has returned 24% in the past one year, not including dividends. Dover has soundly beaten the S&P 500 Index in the same time.

Dividend Growth Backed by Strong Fundamentals

Dover is a diversified industrial manufacturer with annual revenue of approximately $7 billion. It operates in four major segments: Energy, Engineered Systems, Fluids, and Refrigeration & Food Equipment. The energy segment serves primarily oil drillers and producers. Its products are designed for safe and efficient production and processing of fuels. The engineered systems unit designs, manufactures, and services components used in the consumer goods, digital textile printing, and vehicle service industries. In the fluids business, the company is focused on the safe handling of critical fluids across the retail fueling, chemical, hygienic, and oil and gas industries. Lastly, the refrigeration and food equipment division provides energy-efficient systems for the commercial foodservice market.

Breakdown of Revenue and Earnings Contribution by Operating Segment

Despite being hit by several headwinds over the past year, including the strong U.S. dollar, exposure to the oil and gas industry, and declining economic growth in the emerging markets, Dover keeps posting strong profitability each year. Net earnings increased 18% last year, thanks to share buybacks and reductions in capital expenditures. Revenue for the year declined 11%, but the company is off to a better start so far in 2016. Over the first half of the year, revenue declined 5% from the same period last year. It is a good sign that the revenue decline is moderating.

And it should be noted that a significant portion of the revenue decline is due to the strong U.S. dollar, which has reduced competitiveness of U.S. exports and makes internationally generated revenue worth less. Unfavorable currency fluctuations accounted for 1% of the revenue decline in the first half of the year. Management believes that the second quarter will be the bottom for the energy segment and should produce growth in that business going forward. This is based on the increase in North American oil and gas rigs in operation and on climbing commodity prices.

Analysts are increasingly optimistic that Dover will benefit from the recovery in commodity prices and global economic growth. Next year, earnings are expected to grow 16% to $3.94 per share. Based on this forecast, Dover’s payout ratio is projected to be 52% for 2016 and 45% for 2017. This leaves more than enough room for the company to continue increasing its dividend at a high rate.

Over the long term, Dover management believes its strategic initiatives to diversify its business across different geographic markets and industries will provide the company a unique focus and balanced business model. Management maintains the long-term goal of achieving annual organic revenue growth, which excludes foreign exchange fluctuations, in the 3%-5% range. This will be accomplished by internal investments as well as through acquisitions. From 2013-2015, Dover acquired 21 businesses for a cumulative cost of $1.7 billion. Not only does this add to revenue growth, but also Dover opportunistically acquires companies that it believes can produce significant cost synergies.

In addition, the company seeks to maximize productivity by focusing on efficiency in all parts of the business, including supply chain and occasional restructuring. These efforts are expected to generate free cash flow as a percentage of sales greater than 11% each year. Such a high rate of free cash flow conversion allowed the company to raise its dividend for as long as it has.

The Bottom Line

Dover has performed admirably in a very difficult economic climate. It has remained steadily profitable, even though it is facing many challenges. This is a testament to Dover’s strong business model and management team.

Dover stock has a 2.4% dividend yield, which is above the average yield in the S&P 500 Index. Its above-average dividend yield and long track record of dividend growth make Dover an attractive stock pick for income investors.