A sponsored piece of content that takes a deep and historical look into why dividends are so important as part of your equity portfolio’s long-term total returns.

Written by Dr. Ian Mortimer and Matthew Page, CFA, Fund Co-managers.

Introduction

Investors seem to be rediscovering the power of dividends as an important element in the pursuit of long-term total returns. Following the financial crisis of 2008/9 and the resultant fall out, traditional sources of income such as government and corporate bonds and cash, lost their luster. In this paper we aim to show that, for the long-term investor, the power of dividends from equity investing has never been diminished and has in fact been slowly and surely working away, behind the scenes, adding not just appreciation in the form of total returns but can mitigate the effects of both market falls and inflation.

Profits are a matter of opinion, dividends are a matter of fact

Dividends are paid from real earnings and in ‘hard’ dollars – they cannot be manipulated by creative accounting. A dollar paid out to the investor is just that.

If a company has a long history of paying a dividend and is very likely to continue to do so in the future, then it is highly likely that management will begin each new year by first deciding the dividend payout and then thinking about how best to use the rest of the free cash flow. This leaves no room for vanity projects or frivolous uses of shareholders capital. A focused management team that uses the cash available to them efficiently is central to creating a well run – and profitable – company that is able to grow and thrive in the future. Steady and constantly growing dividends can give us a good indication that these elements are in place. Dividend payments can act as a useful barometer to identify companies that are disciplined and efficient in their capital allocation and cash flow management.

There exists an argument, however, that companies who pay a dividend are just struggling to find new growth opportunities and uses for their cash. We think quite the opposite. In the early stages of a company’s life it is quite right that cash is used to establish the business. It is often right that the company continues to re-deploy cash into the business as it moves through the early growth phase and into the maturity phase. Once at maturity, however, when competition has entered the market place and the opportunities for such high growth have diminished, we think it entirely sensible that the company takes stock, and carefully decides to allocate cash to only those projects where it can achieve high returns – and gives the rest back to shareholders. Why would we want management to plough back all the company’s cash regardless of the returns available?

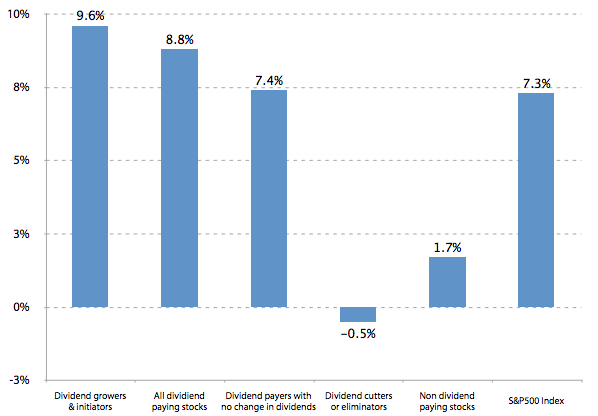

There are always exceptions to any rule, and there will always be examples of companies that have such a unique product or service that they can continue to grow for much longer than the average company. Simple mathematics, however, dictates that even these companies cannot grow forever. Indeed, if we look at the historical evidence for the benefits of company management focusing on dividends we can see a strong relation between total return performance and the company’s approach to dividend policy. The evidence for this can be seen in Figure 1. If we split all the companies in the S&P500 into separate buckets depending on their approach to dividends, we can see that dividend payers have outperformed the broad market, and dividend nonpayers significantly underperformed.

Historical Perspective

Over the long term, dividends have been the main contributors to total return in equity investments. Figure 2 illustrates this point by looking back at the S&P500 returns since 1940. In this period dividends and dividend reinvestments accounted for over 90% of the total return for the index during that time. If you had invested $100 at the end of 1940, this would have been worth approximately $174,000 at the end of 2011 if you had reinvested dividends, versus $12,000 if dividends were not included.

Dividend Cutters and Eliminators represents stocks in the S&P500 that have lowered or eliminated their dividend; Non-Dividend-Paying Stocks represent non-dividend paying stocks of the S&P 500; Dividend Payers with No Change represents all dividend-paying stocks of the S&P500 that have maintained their existing dividend rate; all Dividend Paying stocks represents all dividend-paying stocks in the S&P500; and Dividend Growers and Initiators represents all dividend-paying stocks of the S&P500 that raised their existing dividend or initiated a new dividend.

This is a hugely powerful phenomenon, and something that in recent times seems to have become overlooked as investors try to glean quick profits by capitalizing on short term trading strategies – which come with much increased risks. The average holding period for NYSE-listed stocks between 1950 and 1970 was approximately 6 years. Today it is under 1 year. We think investors should start to think about their investments in the long term once more and return to the ‘buy and hold’ strategies espoused by Benjamin Graham and others – this way investors can attempt to capture the benefits of dividends and dividend reinvestments.

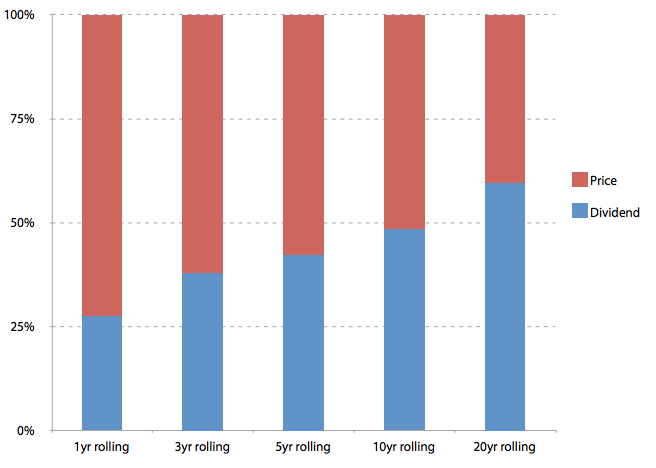

Figure 3 below shows how the importance of dividends to total returns increases with time horizon. For an average holding period of 1 year, dividends accounted for 27% of total returns for the S&P 500 since 1940. If we increase the holding period to 3 years, dividends account for 38%, 5 years it increases to 42%, over a 10 year period it rises to 48%, and with a 20 year holding period dividends account for some 60% of total returns. It is important to note, too, that here we are just looking at the S&P 500 as a whole and not focusing purely on companies that actually pay a dividend. If we did, we think these results would likely be even more striking.

Dividend Characteristics

In the previous section we saw how significant dividends were to the total return of the S&P 500 over the last 70 years. If we further break down this analysis to look at individual decades we can see that the significance of dividends to total returns is not the same in every decade–dividends become much more important in lower growth periods. As Figure 4 shows, the minimum contribution to total return was 25.4% (not an insignificant sum) in 1990, when markets rallied strongly up to the peak of the ‘technology bubble’ at the start of the 2000’s. What we find more compelling, however, is that the importance of dividends to total returns increases dramatically in low growth decades – which are defined by some combination of sluggish economic growth, rising inflation, increasing oil prices, and high unemployment. In low growth periods such as the 1940s and 1970s, dividends accounted for over 75% of total returns.

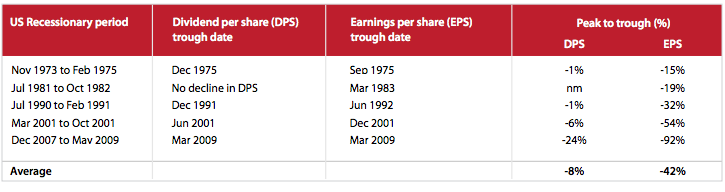

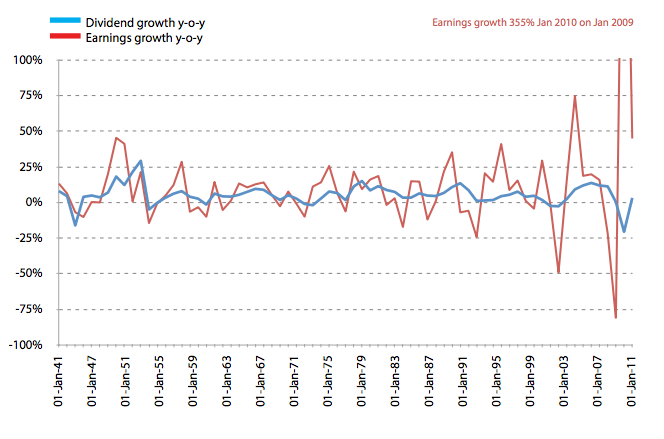

But why should dividends hold up better in difficult markets? There is no magic formula for why this might be the case – companies could stop their dividend payments to reserve cash and protect their balance sheets, and some have in the past. What we see in aggregate, however, is that companies as a group might reduce their dividend payments in particularly austere times, but rarely, if ever, collectively cut their dividend dramatically. The market sees a long history of dividend payments as establishing a company’s credentials and the management team, making significant cuts by company management more unlikely. That is, dividends are a reflection of the long-term earnings power of a company and are therefore set at a level that is sustainable. If we look specifically at the last five recessionary periods in the US, as illustrated in Figure 5, we can see that dividends per share (DPS) for the S&P 500 dropped by 8% on average, compared to an average drop of 42% in earnings per share (EPS) i.e. dividends were cut by less than a fifth of the percentage fall in earnings over those periods. .If we now look at the historic year-on-year growth (or decline) in the earnings relative to dividends per share of the S&P500 we can see that dividends are much less volatile than earnings, as shown in Figure 6. Not only can this provide the investor with a kind of ‘cushion’ during recessionary and/or low growth periods, but it can also allow long term investors to automatically take advantage of short-term periods of low stock prices if they re-invest their dividends throughout the business cycle – a subject we look at in detail in the next section.

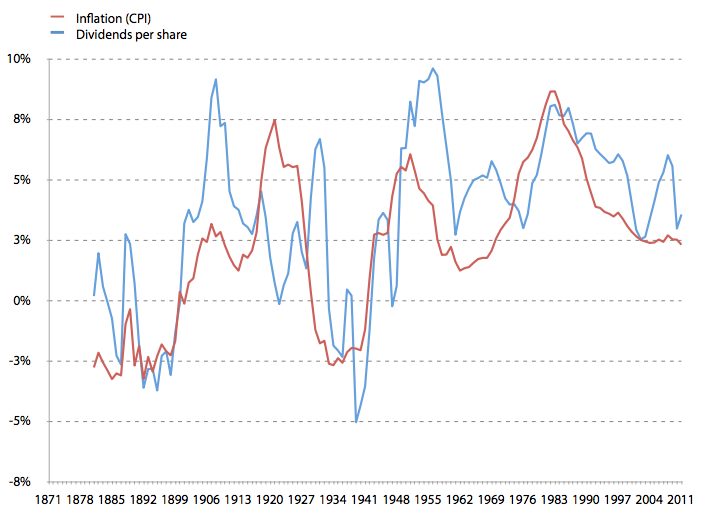

Figure 6 also shows the striking phenomenon that, over the long term, dividend growth is not only positive but is sustained at a reasonably high rate. Over a rolling ten year period, the average growth in the S&P500 dividends per share since the 1940s is 6% per year. Over the same period, inflation, as measured by the consumer price index (CPI) and calculated by the US Bureau of Labor Statistics, grew at 4%. Indeed, if we look at the correlation of dividend growth to inflation over rolling ten year periods, as shown in Figure 7 below, we can see a strong relationship. This shows that investing in divided paying companies can, over the long term, provide an inflation hedge, in the sense that the income received in the form of dividends grows in line (or often at a higher rate) than inflation.

The Benefit of Compounding

A somewhat counter-intuitive phenomenon to dividend investing is that an investor might often be pleased if the share price of the company they own actually decreases in value. But how can this make any sense? The answer is found in the idea that investors should benefit from the fact that, if the company they own continues to pay a dividend despite the fall in share price, the shareholder will receive a greater number of shares upon reinvestment of their income than they would have if the share price had not fallen, i.e. the investor gets to buy more shares for their account per dollar they are re-investing. This combination of income distribution and reinvestment at more attractive valuations can be an extremely effective way to accumulate capital with relatively low risk over the long term.

The key to this approach is three-fold:

- Investors must be prepared to invest over the long term – so the ebb and flow of day-to-day fluctuations in their principal due to short term market movements do not require the investor

to sell down their holdings. - The investor can identify a good quality company that can generate sustainable cash flows through a variety of market environments.

- The company invested in maintains a disciplined approach to its dividend policy and is able to continue to pay a dividend even if its share price is falling.

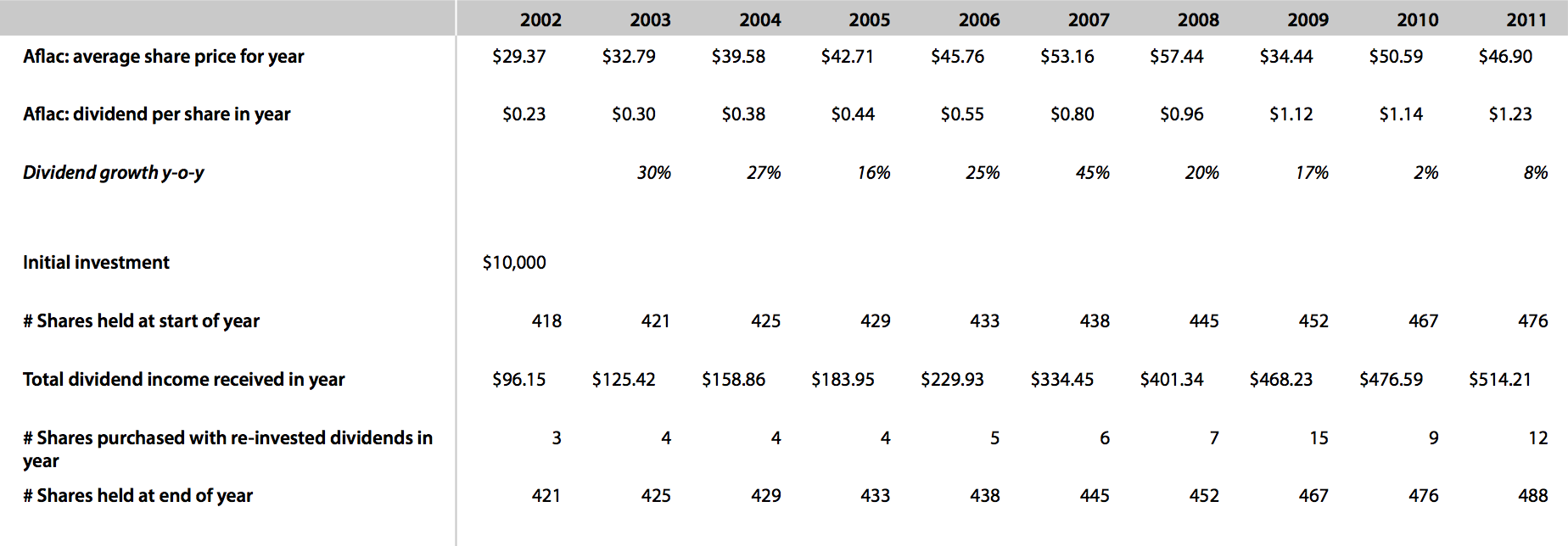

As an example, let’s look at Aflac, an insurance business that has increased its dividend payment every year for the last 28 years. If we imagine we began by investing $10,000 ten years ago, on January 1st, 2002, we can calculate the number of shares we could have bought initially and also the number of shares we could subsequently have bought by reinvesting any dividend payments we received. Figure 8 illustrates the share price performance of Aflac over the period and Figure 9 breaks down how our shareholdings would have changed with the reinvestment of dividends in each year over the period.

Looking at the table we can see three things: (i) Aflac increased its dividend per share payout in every single year, (ii) the number of shares of Aflac that we owned gradually increased throughout the holding period from our initial purchase of 418 shares in 2002 to 488 shares at the end of 2011, and (iii) the amount of shares we were able to buy with our re-invested dividends fluctuated between 3 shares in 2002 and a peak of 15 shares in 2009. So, although the share price fall during the 2008/9 recession was painful when we were looking at our account balance at that time, we actually benefitted from being able to purchase the largest amount of ‘extra’ shares with our dividend income in those years. The compounding benefit of purchasing those shares at much reduced valuations then continued into 2010 and 2011 (and beyond if we remained holders), as the increased share balance provided a greater dollar amount of income in subsequent periods. This quick illustration shows just one example of the powerful compounding effects of dividends and dividend re-investments, but there are others out there for the astute, long term investor to benefit from.

Summary

In our opinion, when looking over the long term, dividends’ contribution to total return is compelling. We therefore believe investors should buck the recent trend for investing in short term themes and instead focus on investments, which by their very nature maintain, and even grow, their income over time. Investors should also recognize that they need not just look at the blue-chip stalwarts to find companies which pay a dividend. We see new companies initiating dividend payments around the globe on a near daily basis. These ‘new’ dividend-paying companies can also provide the investor with the ability to invest to capture a potentially growing income stream – which acts to further compound many of the positive effects such as inflation hedging, or the benefits of compounding over the long-term, we have illustrated in this paper. The key benefit to investors of such a dividend strategy is that it can offer a more systematic approach to reach financial goals over the more common ’buy low, sell high’ strategy.

Read the original article here.

About the Fund Managers

DR. IAN MORTIMER

Co-manager

Joined Guinness Atkinson Asset Management in 2006.

Ian graduated from the University of London in 2003 with a First Class Honors Masters degree in Physics. He then completed a Doctorate in Physics from the University of Oxford in 2006.

MATTHEW PAGE, CFA

Co-manager

Joined Guinness Atkinson Asset Management in 2005 Matthew graduated from New College, University of Oxford, with a Masters degree in Physics. Matthew worked at Goldman

Sachs before joining Guinness Atkinson.

Mutual fund investing involves risk and loss of principal is possible. Investments in foreign securities involve greater volatility, political, economic and currency risks and differences in accounting methods. These risks are greater for emerging markets countries. The Fund also invests in smaller companies, which will involve additional risks such as limited liquidity and greater volatility. The Fund may invest in derivatives which involves risks different from, and in certain cases, greater than the risks presented by traditional investments.

The Fund’s investment objectives, risks, charges and expenses must be considered carefully before investing. The statutory and summary prospectus contains this and other important information about the investment company, and it may be obtained by calling 800-915-6566 or visiting gafunds.com. Read it carefully before investing.

Opinions expressed are those of Guinness Atkinson Funds, are subject to change, are not guaranteed and should not be considered investment advice.

Current and future portfolio holdings are subject to risk.

One cannot invest directly in an index. Index performance is not indicative of Fund performance. Current Fund performance can be obtained by calling 800.915.6566.

Past performance is no guarantee of future results.

Standard & Poor’s 500 Index (S&P 500) is an index of 500 stocks chosen for market size, liquidity and industry grouping, among other factors. The S&P 500 is designed to be a leading indicator of U.S. equities and is meant to reflect the risk/return characteristics of the large cap universe.

Cash Flow Return on Investment (CFROI*) is a valuation model that assumes the stock market sets prices on cash flow, not on corporate earnings. It is determined by dividing a company’s gross cash flow by its gross investment.

Correlation is a statistical measure of how two securities move in relation to each other.

Fund holdings and/or sector allocations are subject to change at any time and are not recommendations to buy or sell any security.

As of 9/30/14, Guinness Atkinson Dividend Builders Fund, previously known as Inflation Managed Dividend Fund, has 2.74% of its holdings in Aflac.

*CFROI is a proprietary metric prepared by HOLT, a division of Credit Suisse. CFROI is a registered trademark of Credit Suisse AG or its affiliates in the United States and other countries. For more information on HOLT, a corporate performance and valuation advisory service of Credit Suisse, please visit their website at https://www.credit-suisse.com/investment_banking/holt/en/index.jsp