At Berkshire Hathaway’s annual meeting in August 2016, Buffett joked about his body being one-quarter Coke at this point.

He went on to say, "There’s no evidence that I will any better reach 100 if I had lived on broccoli and water.” There is no doubt Buffett loves Coke both as a beverage and as a company. In fact, the charismatic owner of 400 million Coca-Cola shares (accounting for 9%) will appear on cans of Cherry Coke in China, where he is well known for his investment style.

The Business of Selling Coke

The Coca-Cola company (KO ) owns or licenses more than 500 nonalcoholic beverage brands that include sparkling or still beverages such as waters, juices, sports drinks, dairy, etc. They account for nearly two billion of the 59 billion servings of all worldwide beverages consumed every day.

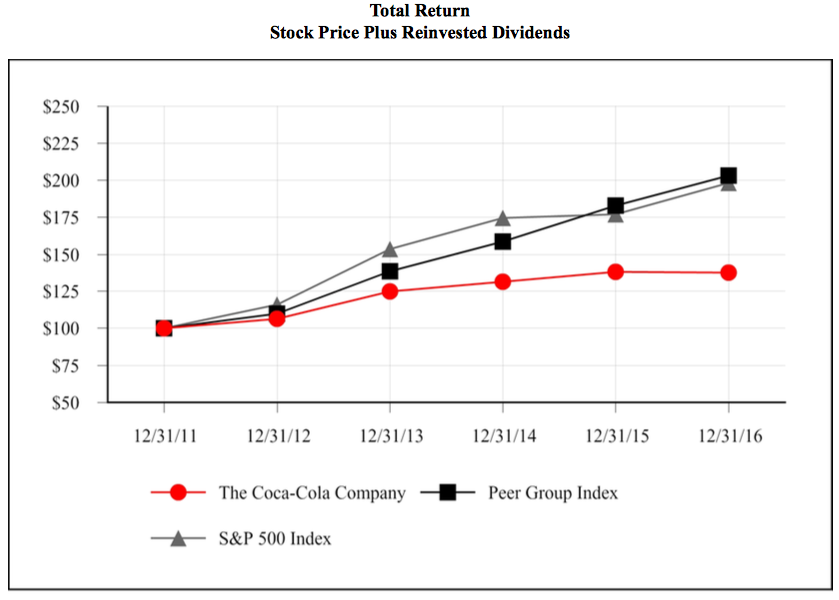

It is a healthy but also a mature business that is struggling to redefine its footprint in an increasingly anti-sugar world. It has seen a steady decline in almost all its financial metrics in the last five years. Sales have gone from around $48 billion in 2012 to $41 billion in 2016. In the same period, gross income has been reduced from $29 billion to $25 billion, net income from $9 billion to $6.5 billion and diluted EPS from 1.97 to 1.49. This explains why the stock price has been unable to keep up with the general market in the last five years, as shown in the graph below. There has not been a significant change in the shares outstanding, which generally helps companies to achieve their financial targets in times of topline and income challenges.

As visible from the graph shown below, in terms of total returns that combine stock returns and dividends, the company has lagged behind its peers and the general market.

Starting in 2014, the company has been actively divesting some of its bottling assets, which are expected to save the company $3 billion in cost reductions over a five-year period. It will make the company more profitable and nimble. Coca-Cola, like others in the industry, has also introduced smaller cans with fewer calories and zero calorie options. The smaller size options allow the company to charge more for the same amount of drink. Sandy Douglas, the president of Coca-Cola North America, said at a conference a couple of years back, “A 12-ounce can traded to a 7-ounce can is a 30% reduction in volume, but it’s an increase in revenue.” As overall soda consumption declines, the company is looking to re-engage with younger customers who are aware of the health risks in sugary drinks.

Coca-Cola is a member of the Dow Jones Industrial Average. Click here for a complete list of the Dow 30 dividend stocks.

Coke vs. Pepsi

No discussion about Coke is complete without a ritualistic comparison with PepsiCo (PEP ). As far as beverages are concerned, the winner is clear as Coca-Cola. It is the world’s largest beverage company that owns four of the world’s top five nonalcoholic sparkling beverage brands: Coca-Cola, Diet Coke, Fanta and Sprite.

Although it is a good taste battle on the dinner table, PepsiCo is not a beverage company like Coca-Cola. In fact, its Frito-Lay segment accounts for approximately 25% of revenue and 41% of operating income. If Quaker Foods is combined to the figures, nearly 50% of the income comes from these two divisions. On the other hand, soda still accounts for 70% of Coca-Cola’s revenues.

Be sure to see how Coca-Cola compares with Pepsi here.

Given the product mix, PepsiCo seems to be better placed for the future. This is reflected in the returns posted by the two companies in the last five years (PEP 71% vs. KO 13%). PepsiCo also has matching dividend credentials with a current yield of 2.85% and growth posted for 44 consecutive years. The dividend growth rates have been similar to Coca-Cola in the last 5 to 10 years. Free cash flow has declined in 2016, but it has increased from $5.77 billion in 2012 to $7.36 billion in 2016.

Just like Coca-Cola, PepsiCo has struggled to grow its topline in the last five years, but it has managed to maintain its gross income, grow its net income ($6.18 billion in 2012 to $6.33 billion in 2016) and diluted EPS (3.92 in 2012 to 4.36 in 2016).

Use the Dividend Screener to find high-quality dividend stocks based upon 16 parameters. You can even screen stocks with DARS ratings above a certain threshold. Stocks with the highest DARS ratings are Dividend.com’s current recommendations to investors.

Coke as an Investment

Coke hit an all-time high in April last year and is currently about 6% below that. Since then, the stock has bounced off the $40 level twice in the previous five months (December 2016, February 2017) and is now in a position to beat a strong resistance level of just under $44.

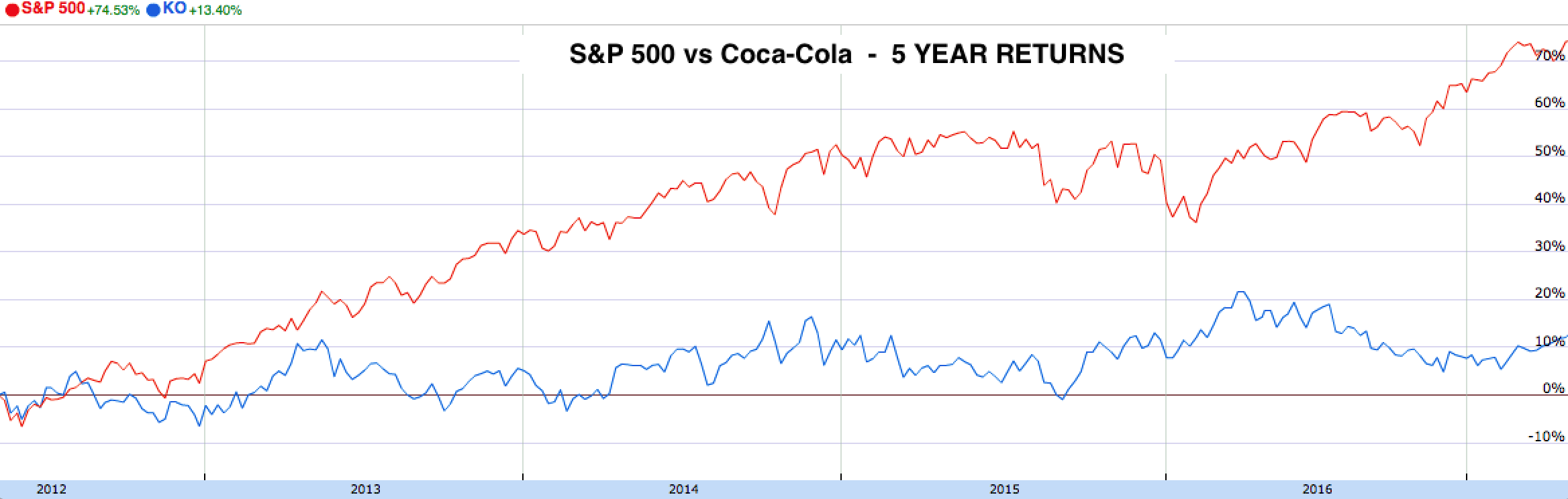

Just like the overall market, Coke has been on a steady rise since early 2009. Tops and bottoms have been higher than previous ones. On a 10 year time-scale, Coke has almost similar returns compared to the S&P 500, but the stock has barely moved in the last five years. While the S&P 500 index has returned nearly 75%, Coke has managed to appreciate just about 13%.

Coke has a strong current dividend yield of 3.39% and has managed to increase its dividends for 54 years in a row. Coke is a comfort stock for long-term passive investors as far as dividends are concerned. There is, however, a cause for concern as the free cash flow has declined more than 20% in the last two years (from $8.21 billion in 2014 to $6.53 billion in 2016). The current dividend payout ratio is also on the higher side at 78.7%. Despite these figures, it is Coca-Cola we are talking about. The dividends are unlikely to stop, but the dividend growth rates might be affected. In fact, it can be seen in the marginally lower dividend growth rates of recent years. All this is still only a technicality because a growth rate of 8.3% in the last five years is still fairly good. Check out the dividend history of Coca-Cola here.

Coke currently seems to be expensive in simple valuation terms. It has a PE ratio of around 30, which is higher than peers like PepsiCo, Dr. Pepper Snapple (DPS) (demerged from Cadbury Schweppes in 2008) and general market indices like the Dow Jones Industrial and S&P 500.

Want to know how Coca-Cola was able to increase its dividend for more than 50 years? Check it out here.

The Bottom Line

Coca-Cola has spent nearly $4 billion in each of the last two years with a renewed focus on its core brand (instead of individual products) and continues to find ways to make itself more profitable. While other companies are focusing on diversifying their offering away from sugary drinks, the company seems to have decided to further solidify its leadership position around its core strength.

It is too early to say whether this kind of differentiation will yield results in the long run but it is exciting to see a mature (100,000 people) company having the courage to dig deep and go back to its roots when the world around it is changing.

Stay up to date with next week’s major corporate changes regarding dividends in our News section on Dividend.com.