Tobacco stocks have long been relied upon by investors for high levels of cash returns. Reynolds American (RAI) is no exception. It recently increased its dividend by 10% and added $2 billion to its share repurchase program. The new quarterly dividend rate will be $0.46 per share, or $1.84 per share on an annualized basis. The next quarterly distribution will be paid Oct. 3, to shareholders of record on Sept. 12. This dividend increase elevates Reynolds American’s current dividend yield to an attractive 3.6%.

Reynolds American’s $2 billion buyback represents approximately 3% of its market capitalization and, therefore, should be a meaningful tailwind for future earnings growth. The buyback is expected to be completed over the next two years.

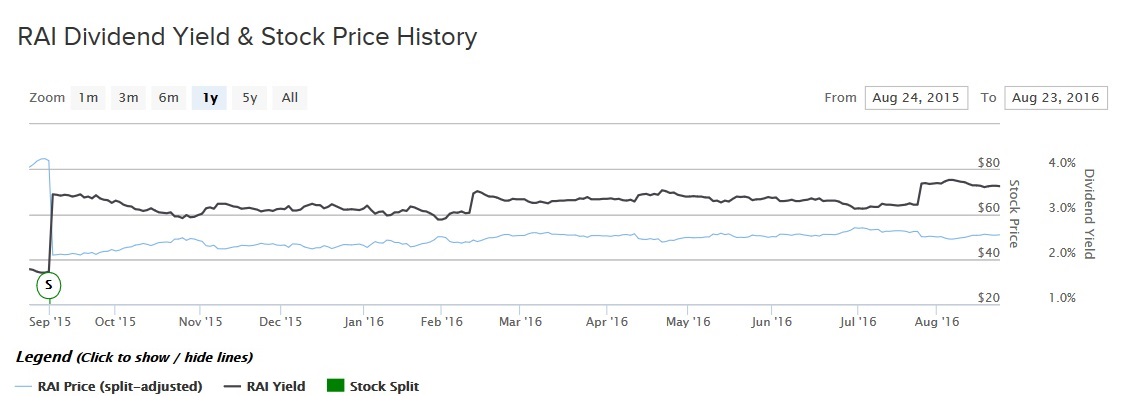

Reynolds American stock, like the tobacco industry more broadly, has performed very well over the past one year. Based on its Aug. 24 closing price, the stock returned 26% in the trailing 12-month period, and that does not include its above-average dividend payments in that time. Its outperformance of the S&P 500 over the past one year is highly impressive, and the stock should be looked at favorably by income investors.

Huge Free Cash Flow Supports Dividends and Buybacks

Reynolds American is a giant in the tobacco industry. Now that it has acquired Lorillard, the company has a large portfolio of brands across both combustible and noncombustible products. Some of its major cigarette brands include Newport, Camel, Pall Mall, and Natural American Spirit. It also has the second-largest smokeless tobacco products business, under the Grizzly and Kodiak brands. Finally, Reynolds American is investing heavily in growth products for the future, including the VUSE brand of digital vapor cigarettes. These brands command significant market share. Last quarter, retail share of Reynolds American’s tobacco segment increased 0.1% to 32.2%.

Tobacco companies have historically paid very high dividend yields, well above the market average yields, because of the strength of the underlying business model. Tobacco companies are not very capital intensive; they enjoy massive economies of scale, which keeps manufacturing and distribution costs low. In addition, they are banned from advertising in the U.S., which keeps marketing expenses low. And they sell products that are addictive. This gives tobacco companies a high degree of pricing power.

These qualities are the reason tobacco companies generate very high levels of free cash flow each year. For example, last year Reynolds American generated $3.38 billion of operating cash flow, after excluding the $3.2 billion one-time divestiture gain incurred during 2015. This compares to just $174 million in capital expenditures for the year. The end result is that the company reported an adjusted free cash flow level of $3.2 billion in 2015, which represented 30% of total revenue last year. Reynolds American has consistently generated very high levels of free cash flow as a percentage of sales for the past several years, which allows the company to return huge amounts of cash in the form of dividends and share repurchases.

Free Cash Flow and Revenue

Going forward, Reynolds American intends to continue increasing sales, both organically due to new products and from acquisition. In 2014, Reynolds American bought fierce competitor Lorillard for $25 billion — a massive deal that brought together the number two and number three tobacco companies in the U.S. — to compete more directly with industry leader Altria Group (MO ).

With the acquisition, Reynolds American should be able to squeeze out significant cost synergies, since Lorillard is a nearly identical company with virtually the same processes in production and distribution. Many duplicated costs can be eliminated by combining the two companies. And this has fueled strong results so far this year. Reynolds American’s adjusted earnings rose 15% over the first half of 2016, compared with the same period last year, due primarily to cost cuts and price increases. Cost savings resulted in the company’s first-half operating profit margin rising by 5.8 percentage points from the first half last year. Going forward, the company forecasts even greater earnings growth for the full year, thanks to these initiatives. Management has projected full-year adjusted earnings per share to increase 14%-18% in 2016.

The Bottom Line

Reynolds American has a very shareholder-friendly management team that is committed to growing the dividend over time. The 10% increase comes after a 16% dividend increase in February. The company is increasing its dividend again because it has raised the target payout ratio for the company. Going forward, Reynolds American intends to maintain a payout ratio of 80% of annual earnings, up from 75% previously.

Income investors are in a difficult position. With interest rates still near historic lows, it is not easy to find high dividend yields. But the tobacco sector is still a good source of yield for investors looking for income, and Reynolds American is one of the industry leaders.