Retail is among the most disliked industries in the stock market right now. Analysts are very bearish on physical retailers, essentially throwing in the towel. The fear is that Internet retail, led by Amazon.com (AMZN), will continue to take market share due to the convenience of its fast shipping, at-home delivery, and low prices, serving as the death knell for traditional bricks-and-mortar retail.

But when it comes to TJX Companies (TJX ), the sentiment does not match reality. TJX remains solidly profitable and is growing sales and earnings at a rapid pace. Its stock price is up 11% in the past one year based on its March 31 closing price. The stock has outperformed both its industry peers as well as the broader market in that time.

The reason TJX has done so well in a relatively poor climate for retail is because of its focus on keeping prices low. In addition, TJX has several strong brands that continue to remain popular with consumers. Reflecting its success, TJX recently raised its dividend by 24% and also announced a new $1.5-$2 billion share buyback authorization.

Get all the latest dividend increases in our payout tool available for premium members.

Strong Brands, Buybacks Provide Earnings Growth

TJX is a major retailer in the United States. It is the parent company of the TJ Maxx, Marshall’s, and Home Goods stores. TJX’s success is due to strong growth across its brands. In 2015, the company grew total sales by 6% to $30.9 billion, and comparable sales by 5%. Comparable sales are a crucial metric for retailers, measuring growth at locations open at least one year. It indicates the staying power of a retailer’s brand. Comparable sales growth accelerated in 2015 from the previous year, in which it grew by 2%. Earnings per share jumped 5% for 2015 to $3.33 per share.

The company has enjoyed a prolonged period of success thanks to these brands. In fact, 2015 marks 20 years in a row of increases in both comparable sales and earnings per share. Going forward, TJX should have little trouble growing earnings further. This will be due to projected sales growth as well as the benefit of the company’s new stock buyback program.

For fiscal 2017, TJX expects diluted earnings per share to be in the range of $3.29 to $3.38. That range would represent a 1% decrease at the low end, to a 2% increase at the high end, from the previous year’s $3.33 in EPS. Foreign currency exchange will have a 4% negative impact on EPS growth, meaning TJX’s organic results will show more satisfactory growth. Comparable store sales are expected to grow once again by 1% to 2% year over year.

The new buyback authorization represents approximately 4% of the company’s outstanding shares, which is a significant repurchase that will provide a tailwind to EPS. The stock repurchase program is the 17th such program approved by the Board of Directors since 1997. Over that period, TJX spent approximately $16.3 billion on the repurchase of its own shares. Share repurchases are a significant piece of its earnings growth.

Dividend Growth Expectations

TJX has been an excellent dividend grower for many years. Its new annualized dividend rate of $1.04 per share yields 1.4% right now. That’s a below-average yield, but over time the stock can make up for this with strong dividend growth. In fact, this raise represents 20 years in a row of consecutive dividend growth for the company. According to the company, in that time, it has increased its dividend by 23% compounded annually. That is a very high rate of dividend growth that helps make up for its low current yield.

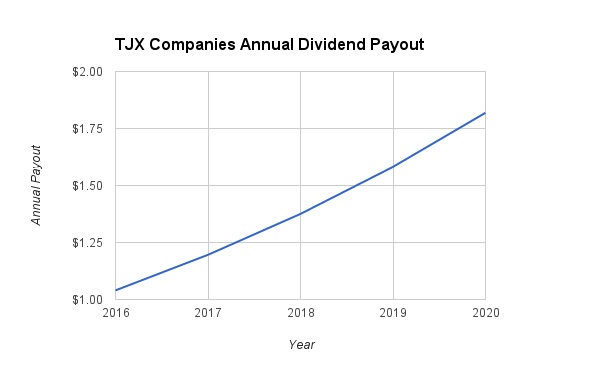

In addition to its sales and earnings growth, TJX maintains a low payout ratio, which also contributes to its high dividend growth. Its new dividend represents just 31% of trailing earnings per share. The company can easily continue to raise its dividend at double-digit percentage rates each year and still maintain a comfortable payout ratio. For example, while investors should conservatively project less dividend growth than in recent years, Dividend.com expects TJX to raise its dividend by at least 15% per year over the next several years. By 2020, that would take TJX’s dividend to $1.82 per share, which still represents barely more than half of its 2015 earnings.

The Bottom Line

The poor performance of most retail stocks indicates that physical retail is dead. However, judging by TJX’s financial performance and increasing cash returns, that does not appear to be true for this company. While Internet retail is indeed having a negative effect on certain underperforming retailers, TJX is still highly successful. The stock has a below-average dividend yield, which may not be attractive to certain income investors who desire current income, but nonetheless, TJX is an excellent dividend growth stock.