Realty Income (O ) calls itself ‘The Monthly Dividend Company’ because it pays its dividend every month, which allows its investors to compound their wealth even faster than they would with quarterly distributions. Realty Income is a real estate investment trust, or REIT, and maintains a long history of dividend growth. O has made 549 consecutive monthly dividend payments and has raised its monthly dividend 85 times since its initial public offering in 2004.

Its track record of dividends is impressive. According to the company, it has paid over $3.9 billion in dividends to investors over the past 47 years. Since its 2004 IPO, the company has raised its dividend by 5% per year, compounded annually.

On March 21, Realty Income declared a monthly dividend of 19.9 cents per share. The same monthly dividend last year totaled 18.95 cents per share. The company has increased its dividend 5% year over year. Get all the latest dividend increases/decreases in our payout tool available for premium members.

Based on its most recent closing share price, Realty Income’s new annualized dividend rate provides a 3.8% dividend yield. Realty Income is a top pick in the REIT sector and is an excellent dividend stock.

Tenant Portfolio, Cash Flow Support Dividend Growth

One of the major contributors to Realty Income’s steady dividend growth is its differentiated business model. Realty Income owns more than 4,500 properties rented under long-term leases. These properties are primarily rented to retail tenants that come from various industries such as distribution centers, health and fitness facilities, and drugstores. Realty Income is highly diversified—its tenants span 47 industries, and in all there are 240 commercial tenants. A unique aspect of Realty Income’s business model is that it engages in “net” leases, meaning the tenant is responsible not just for paying rent every month, but also for covering the major operating expenses such as taxes, maintenance, and insurance.

Realty Income’s strong business model is displayed through its growth in funds from operation, or FFO. This is a non-GAAP equivalent to earnings per share that is a better measure of an REIT’s financial performance than traditional GAAP earnings per share. Last year, Realty Income grew revenue by 9.6% to $1.023 billion. Realty Income reported FFO per share in 2015 increased 7.4% to $2.77, as compared to $2.58 earned the previous year.

Realty Income maintains excellent portfolio metrics. At the end of 2015, portfolio occupancy was 98.4%, unchanged from the same time the year before. The company has a weighted average remaining lease term of approximately 10 years. Further, Realty Income has pricing power—the same store rents on 3,636 properties under lease increased 1.3% last quarter.

The biggest risk Realty Income investors need to keep in mind moving forward is interest rate risk. This widely affects REITs because they operate highly debt-heavy capital structures, and when rates go up, interest expense goes up. This threatens to raise Realty Income’s cost of capital, which would impact its growth. But this interest risk seems to be contained. First, the U.S. Federal Reserve has reiterated that the pace of interest rate raises will be slow and gradual. Consequently, Realty Income will have plenty of time to prepare its balance sheet.

Realty Income has ample liquidity to handle rising interest rates. The company has ample access to capital in both the equity and debt markets. For example, in January, the company sold 11 million shares, the proceeds of which were used to pay down debt. In addition, as of December 31, 2015, Realty Income had a borrowing capacity of $1.76 billion available on its revolving credit facility. Interest expense decreased last quarter by $7.1 million, to $52 million. This decrease was driven by less overall debt in the balance sheet. The company repaid $150 million of bonds and approximately $200 million of mortgages last year. In the future, Realty Income’s interest expense should not grow at a dangerous rate because the company pays down debt.

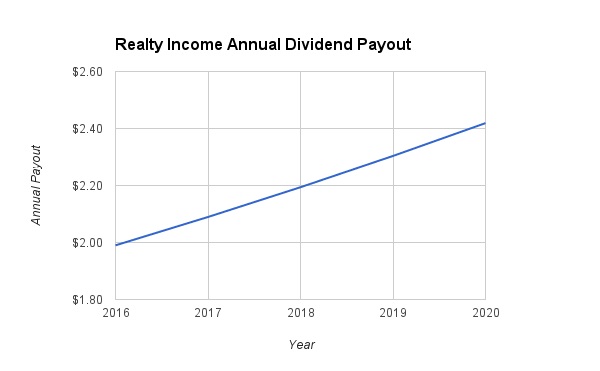

Management expects another 2% to 4% growth in FFO in 2016, which should provide more than enough growth to continue increasing the dividend. Going forward, investors should expect the company to increase its dividend by 4% to 6% per year, in-line with its historical average. Assuming 5% annual dividend growth rate, Realty Income’s dividend will grow to $2.42 per share by 2020.

The Bottom Line

With such a long track record of consistently paying dividends, it is clear that Realty Income has stood the test of time. It has continued to pay, and increase, its dividend regularly for decades. This was even true during periods of very high interest rates and also during periods of economic downturn and recession. Realty Income has a recession-resistant business model and a high dividend yield. For these reasons, dividend investors should not avoid Realty Income simply because of the prospect of rising interest rates. Realty Income is a highly attractive stock pick for dividend investors.