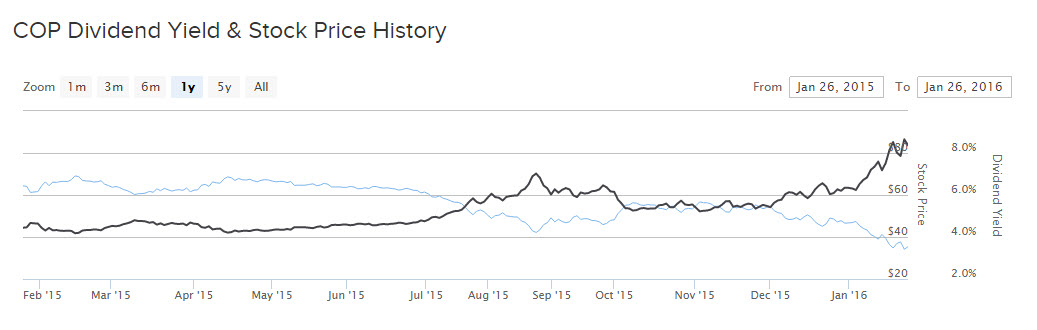

Investors are not surprised that energy stocks are going down. The decline in oil and gas prices over the past two years has caused the entire energy sector to underperform the market in that time. The latest shock to the markets is that oil major ConocoPhillips (COP ) has cut its dividend by 66%, shocking investors. Shares of ConocoPhillips are down 24% in just the past one month, and the selling has intensified since COP decided to cut its dividend.

The reason investors were so surprised by the news is because ConocoPhillips management pledged repeatedly that they would not cut the dividend. In quarterly reports and conference calls, management reiterated that maintaining the dividend was among the top financial priorities for the company. Since ConocoPhillips had held on this long throughout the oil downturn without cutting its dividend, investors clearly hoped COP would make it through.

However, management’s claim that the dividend could survive were not backed up by the underlying fundamentals. ConocoPhillips had to cut its dividend because its business model was overly exposed to falling oil prices, even more so than its peer group.

Upstream vs. Integrated

ConocoPhillips is an independent upstream company. That means it is predominantly engaged in the discovery, exploration, and production business. As such, it is highly reliant on a supportive commodity price to generate cash flow and earnings. This is different than most other Big Oil majors such as Exxon Mobil (XOM ). Exxon’s business model is referred to as integrated, meaning it has a large downstream refining business in addition to its upstream operations.

The refining business acts differently than the upstream exploration and production. When oil prices decline, refining actually tends to improve because as the price of oil declines, input costs become cheaper for refiners. This expands refiners’ spreads and profit margins. In 2012, ConocoPhillips spun off its downstream business, which now trades independently as Phillips 66 (PSX ).

This matters greatly to current shareholders of just ConocoPhillips because the company no longer has protection against falling oil prices. For integrated companies like Exxon, the downstream business is providing billions of dollars in earnings that are helping to offset the declines on the upstream side. ExxonMobil earned 67 cents per share last quarter, down by half year over year. That at least beat analyst expectations, which called for 63 cents per share. Its downstream unit was a source of strength in 2015. Downstream earnings more than doubled for the year, to $6.5 billion.

Without its refining unit, ConocoPhillips is reporting huge losses. The company lost $3.5 billion in the fourth quarter alone, which amounted to a loss of $2.78 per share for the quarter. Meanwhile, analysts expected a loss of just 65 cents per share. ConocoPhillips lost $3.58 per share for the full year 2015. Therefore, it is not surprising that the company finally cut its dividend. It has resorted to cost cuts and asset sales to raise the necessary cash to maintain its dividend thus far, including a 14% reduction in 2015 capital expenditures and $2 billion of asset sales for the year. But these actions can only accomplish so much; cost cuts cannot continue forever. Sooner or later, a company that is losing money cannot maintain its dividend.

Resetting Dividend Expectations

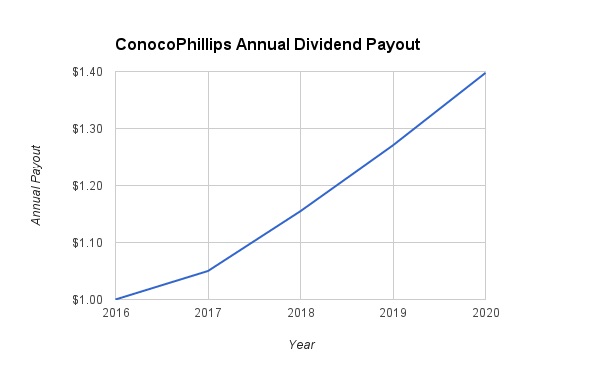

ConocoPhillips announced that its new dividend will be a 66% reduction to $1 per share annualized. Because of this, investors need to significantly reduce future dividend expectations for the company. It is very unlikely that ConocoPhillips will return to dividend growth without a significant increase in the price of oil. As a result, investor expectations for the dividend will be highly correlated to the expectation for oil prices.

If oil can maintain a $50 to $60 price level by the end of the year, it stands to reason ConocoPhillips could at least raise its dividend in 2017 and beyond. The company states that its net profits are reduced by $85 million to $95 million for every $1 per barrel change in Brent crude, and by $40 million to $45 million for every $1 per barrel fluctuation in West Texas Intermediate crude. If WTI can increase roughly $20 to $30 per barrel from current levels, it will restore approximately $800 million to $1.3 billion in annual earnings for the company.

Under these assumptions, we are therefore modeling no dividend growth this year from the $1 level, 5% dividend growth in 2017, and 10% dividend growth in 2018-2020. ConocoPhillips’ 2020 dividend payout reaches $1.40 per share in that scenario, which would represent a 4.2% yield based on its current stock price.

The Bottom Line

ConocoPhillips’ decision to cut its dividend by two-thirds was a shock to investors. The new dividend yield is just 3%, which is not very attractive in relation to the industry. There are plenty of other stocks, such as Exxon, that offer higher current dividends, and the risk of a dividend cut for Exxon is much lower. As a result, income investors should avoid the stock, and current shareholders may want to consider replacing ConocoPhillips with a higher-yield stock that has a more secure payout.