For decades, long-duration bonds served as a foundational stabilizer within diversified portfolios. They provided steady income, capital appreciation during economic slowdowns, and a reliable counterbalance to equity volatility. But the unusual macroeconomic dynamics of the past several years- marked by aggressive rate hikes, persistent inflation, and historically poor bond performance- disrupted that relationship. Many investors questioned whether long-term bonds could still serve their traditional purpose.

However, current attractive valuations on long-duration bonds suggest the potential to regain their role as a portfolio diversifier once again.

Long-duration bonds could be an excellent asset class for portfolio diversification in the coming quarters, offering both the potential for capital appreciation and essential downside protection should the economic cycle shift.

Understanding the Bond Market’s Recent Struggles

The past few years have been some of the most challenging in modern fixed-income history.

Following an extended period of ultra-low interest rates, the Federal Reserve embarked on its most aggressive rate-hiking campaign in four decades to combat surging inflation. The rapid rise in yields led to significant declines in bond prices, particularly in long-duration segments that are highly sensitive to interest-rate changes. Many investors experienced unexpectedly deep drawdowns in parts of their bond allocation, shaking confidence in the asset class.

According to the asset manager, Wellington, the main bond benchmark – the Bloomberg Aggregate Index (Agg) – has not generated a real return since early 2010. This represents a lost decade and a half after accounting for inflation. 1

In addition, bonds have done a poor job concerning their other main function- portfolio ballast. They simply haven’t protected capital during downturns. Wellington notes that during the rate-induced market sell-off of 2022, banking crisis of 2023, and more recently, the Liberation Day Tariff woes of early 2025, bonds didn’t protect investors’ capital during these downturns. They sank right along with equities.

The distress and losses currently affecting the broader bond market are notable because they stem from factors other than typical drivers, like weakening credit fundamentals, recessionary pressures, or a major economic shock. It has been the sheer speed and magnitude of interest rate moves that caused instability. At the same time, inflation reached levels not seen since the early 1980s, undermining the purchasing power of fixed coupon payments and further dampening sentiment toward long-duration investments.

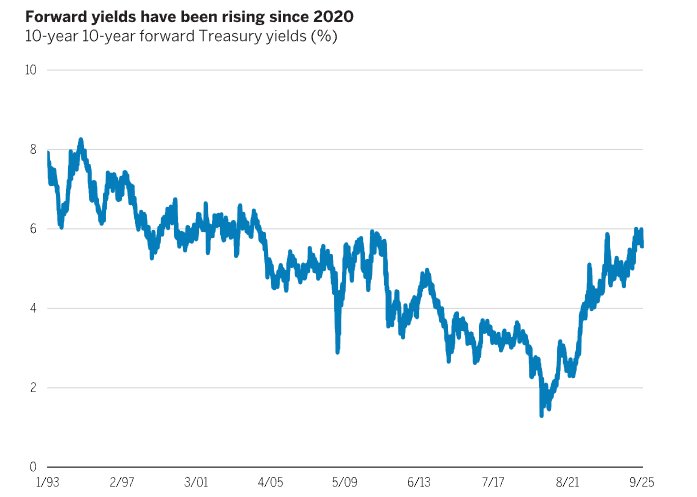

The result is that many investors have given up on longer-maturity fixed income. This has pushed forward yields higher, as demonstrated by this chart.

Source: Wellington

Today’s High Yields May Not Last

However, monetary policy seems to be approaching an inflection point. This brings up a key question for investors. And that’s whether long-duration bonds can reclaim their historic role as a great portfolio diversifier, protector of capital, and produce strong total returns.

The answer is increasingly yes. It is unlikely that the currently high yields will continue indefinitely.

Yields on long-term Treasuries, investment-grade corporates, and long-duration taxable municipals have recently climbed to levels more in line with historical averages, moving past the artificially low environment that followed the global financial crisis. Despite this increase, several factors suggest that these yields could decline over the medium term.

For starters, the inflation spike that destabilized bond markets has eased meaningfully. While inflation remains above pre-pandemic levels, supply chains have stabilized, consumer demand is normalizing, and wage growth is slowing. Moreover, demographics, technological innovation, and global competition continue to exert downward pressures on long-term inflation, despite short-term shocks.

Looking at breakeven points between 30-year Treasuries and 30-year Treasury Inflation-Protected Securities (TIPS), we currently arrive at 2.25%. This level is comparable to inflation pricing before the COVID-19 pandemic and significantly below the figures observed in the years preceding the global financial crisis. All in all, the markets are pointing to muted inflation.

Additionally, long-duration bonds offering 4%–5% yield or more create a strong incentive for institutional investors particularly pensions, insurers, and global fixed-income buyers to lock in income. It is a crucial consideration, particularly in the current environment of decreasing interest rates. This additional demand can help moderate yields over time despite any fiscal tailwinds.

The current high yields offer investors a substantial margin of safety, one that is considerably greater than what was available during many recent economic downturns. This provides an additional cushion. A combination of all these factors creates a very bullish picture for long-duration bonds, enabling them to be core diversifiers once again.

Long-Duration Bonds in Modern Portfolios

With the current environment favoring long-duration bonds, price appreciation, and the ability to lock in current high yields, investors should consider loading them up in their portfolios. Luckily, this is a pretty easy thing to do. You can easily buy long-dated Treasuries directly from the government or through any brokerage account. The same could be said for corporate bonds or munis.

However, like many asset classes, using an ETF has plenty of benefits, such as lower investment minimums and diversification. Adding a long bond ETF to a portfolio could provide a return to the diversification role that these bonds once had.

Long Bond ETFs

These funds were selected based on their exposure to longer-dated bonds. They cover a wide range of bond types and are sorted by their one-year total returns, which range from 0.4% to 7.8%. They have assets under management of $7M to $49B and expenses of 0.03% to 0.15%. They are currently yielding between 3.8% and 5.8%.

| Ticker | Name | AUM | YTD Total Ret (%) | Yield (%) | Exp Ratio | Security Type | Actively Managed? |

|---|---|---|---|---|---|---|---|

| UTEN | US Treasury 10 Year Note ETF | $224M | 7.8% | 3.8% | 0.15% | ETF | No |

| VGLT | Vanguard Long-Term Treasury ETF | $14.3B | 5.8% | 4.3% | 0.03% | ETF | No |

| SPTL | State Street SPDR Portfolio Long Term Treasury ETF | $11.9B | 5.8% | 4% | 0.03% | ETF | No |

| BBLB | JPMorgan BetaBuilders U.S. Treasury Bond 20+ Year ETF | $7.4M | 5.5% | 5.1% | 0.04% | ETF | No |

| TLT | iShares 20+ Year Treasury Bond ETF | $48.8B | 5.2% | 4.4% | 0.15% | ETF | No |

| EDV | Vanguard Extended Duration ETF | $5B | 2.5% | 4.8% | 0.05% | ETF | No |

| ZROZ | PIMCO 25+ Year Zero Coupon U.S. Treasury Index ETF | $1.72B | 1.4% | 4.5% | 0.15% | ETF | No |

| GOVZ | iShares 25+ Year Treasury STRIPS Bond ETF | $300M | 0.4% | 4.7% | 0.15% | ETF | No |

The challenges of recent years temporarily disrupted the traditional role of long-duration bonds, but the macroeconomic environment is beginning to tilt back toward conditions that historically favored them. As inflation moderates, growth slows, and central banks approach the end of tightening cycles, long-duration bonds offer an attractive combination of yield, capital appreciation potential, and diversification.

Bottom Line

For investors seeking stability, balance, and strategic opportunity, long-duration bonds are once again worth a meaningful place at the table. With yields still elevated, now may be a rare opportunity to lock in long-term income while preparing portfolios for the next phase of the economic cycle.

1 Wellington Management (October 2025). Long bonds could become a diversifier once again