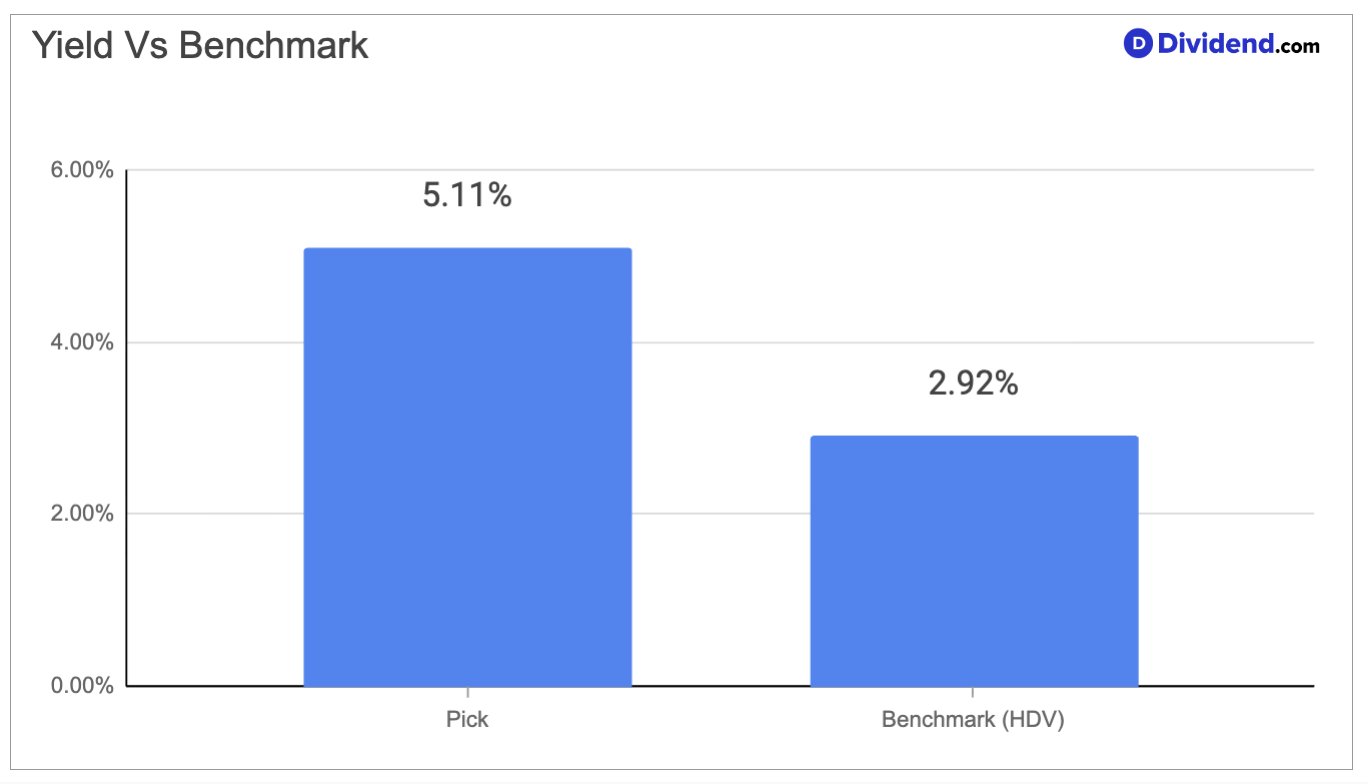

A large-cap real estate investment trust specializing in single-tenant, triple-net-leased commercial properties is delivering a forward dividend yield of 5.11%, paid every month, to shareholders who have grown to appreciate its consistency and scale. This REIT operates across more than 15,500 properties, drawing rent from tenants in essential, location-sensitive industries such as grocery, convenience stores, home improvement, dollar stores, and quick-service restaurants — businesses that need reliable, physical space to serve customers regardless of economic conditions. That structural positioning, spanning over 90+ industries and increasingly global in scope, makes the monthly income stream both predictable and defensible, even as commercial real estate broadly faces rate-related headwinds. The yield of 5.11% sits in the top 40% of all dividend-paying stocks, a meaningful signal of income competitiveness within the equity landscape.

Behind that yield is a business model designed to limit the landlord’s exposure to operating costs, with tenants covering most property-level expenses under triple-net lease structures. This cost-sharing arrangement strengthens cash flow predictability and has historically enabled the company to sustain, and modestly grow, its monthly dividend through varying market cycles.

The company faces some headwinds, notably an elevated debt load and a relatively short dividend-increase track record of 1 year, both of which introduce caution alongside the compelling income proposition. Interest expense is a consideration in any rate-sensitive environment, and management has proactively reduced exposure to specific tenants facing financial stress. These are not disqualifying risks, but they require investors to weigh yield attractiveness against balance sheet discipline. The company’s 9% projected FFO-per-share growth for fiscal year 2026, alongside record investment volume and near-perfect portfolio occupancy of 98.9%, offers meaningful reassurance about operational momentum and the durability of distributions going forward.

This analysis reflects our decision to increase the position in the Best Monthly Dividend Stocks Portfolio. The combination of a top-40% forward yield, accelerating investment activity targeting $8 billion in 2026, and a globally diversifying platform makes this triple-net REIT a compelling core holding for income-focused investors who prioritize monthly cash flow with a reasonable margin of safety.