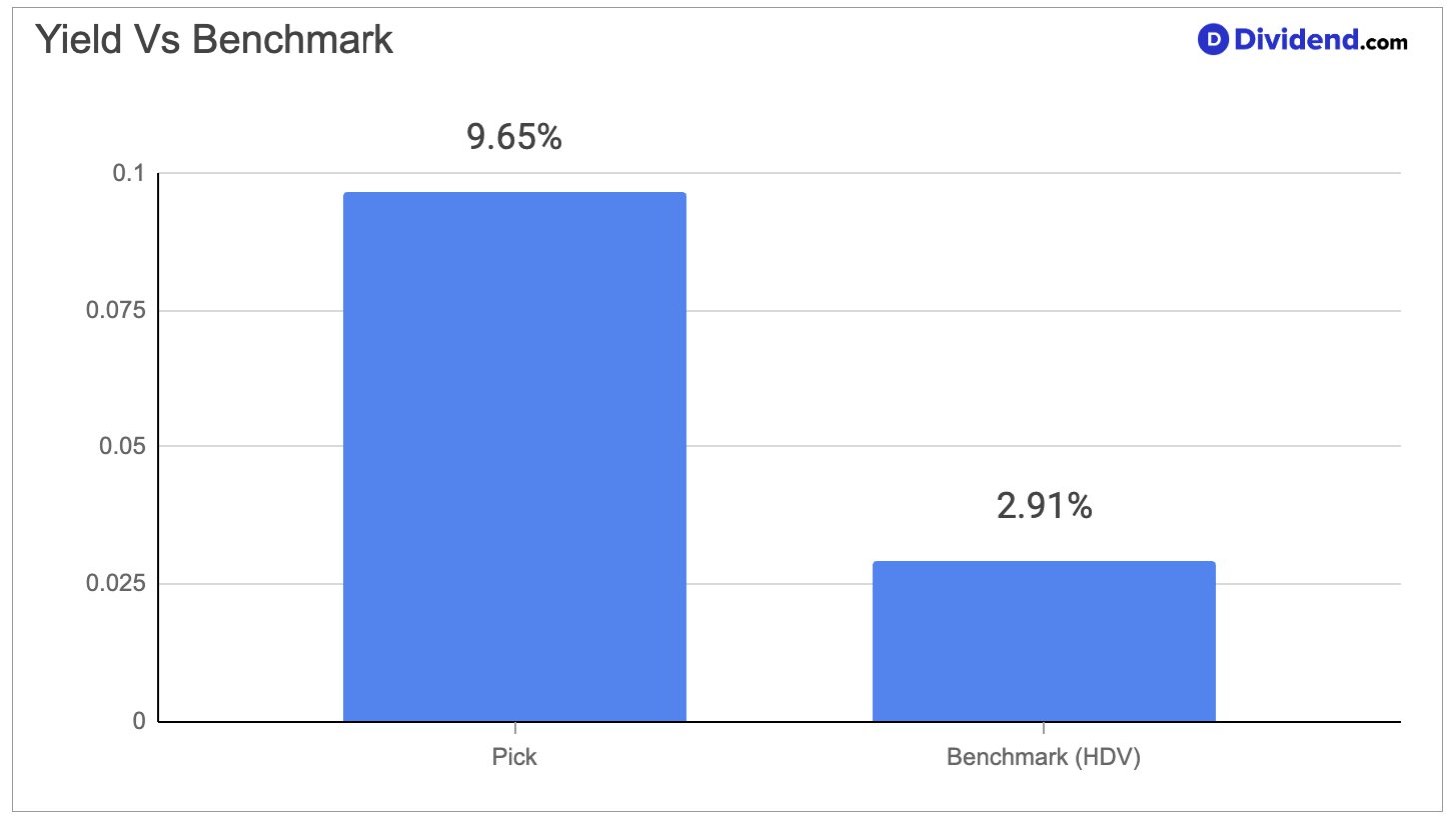

A net-lease real estate investment trust operating across industrial and office properties in suburban United States markets is quietly building one of the more compelling income cases in the REIT space, and its near-10% forward dividend yield is the headline number that commands attention. That yield, currently sitting at 9.65% on an annualized payout of $1.20 per share, is paid every single month — a structural advantage for income-focused investors managing cash flow needs. The trust has been deliberately repositioning its portfolio away from office exposure and toward industrial properties, targeting at least 70% industrial concentration by the end of 2026, and the first quarter of 2026 showed that operational momentum is building in exactly that direction.

The company collected 100% of cash-based rents in the most recent quarter, maintaining a streak of perfect rent collection that speaks directly to the quality of its tenant base and the durability of the long-term net lease structure it uses. With total operating revenues growing from $37.5 million to $41.9 million year over year, and an acquisition pipeline of $300 to $350 million under active review, this is a trust that is generating income today while constructing the foundation for a larger, more focused industrial portfolio tomorrow. Its weighted average lease term of 7.3 years provides long-duration visibility into future cash flows, reducing the near-term leasing uncertainty that plagues shorter-duration commercial real estate strategies. The trust targets smaller properties in the $10 million to $50 million range in secondary markets — a niche where competition from institutional buyers is lower, deal pricing is more disciplined, and the company’s ability to act as an all-cash acquirer creates a genuine transactional advantage.

Key risks include the remaining office exposure being worked down, near-term debt maturities that are manageable but worth monitoring, and a 3-year dividend growth record of flat versus peers who have averaged modest growth. The trust also carries elevated short interest relative to its peer group, reflecting some market skepticism about its transition timeline and valuation discount.

This combination of a high monthly yield, a credible industrial repositioning strategy, and disciplined acquisition activity makes a strong case for inclusion in the Best Monthly Dividend Stocks Portfolio. We have increased our position in this net-lease REIT because the income profile is strong, the operational execution is consistent, and the portfolio transformation is progressing on schedule.