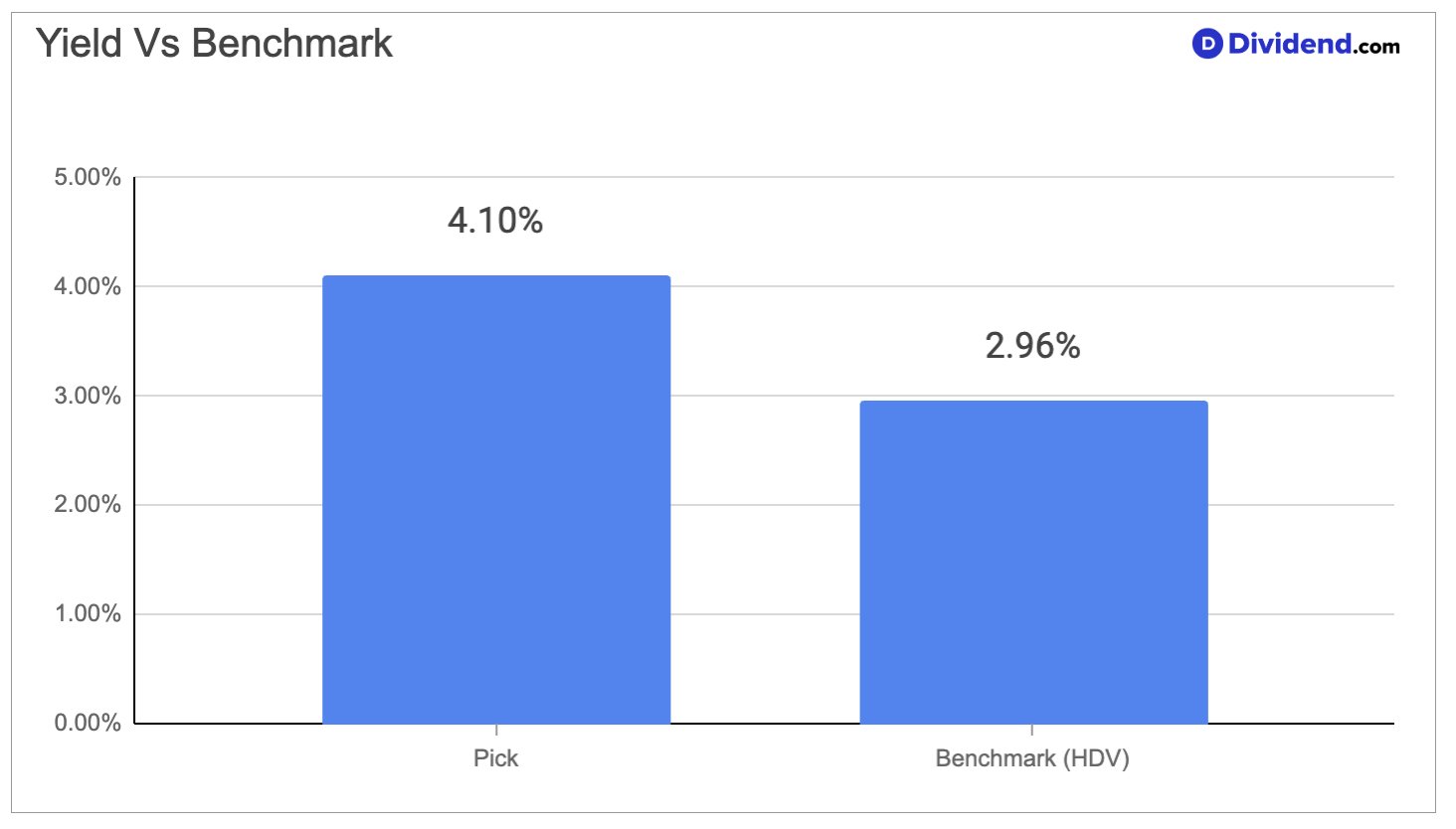

This retail real estate investment trust delivers a forward yield of 4.10 percent paid monthly. It owns more than 2,500 net-leased properties totaling 55.5 million square feet across all 50 states. Long-term triple-net leases to omni-channel retailers in grocery, home improvement, convenience, and specialty segments generate predictable rental income with minimal operating exposure.

Fourth quarter 2025 results showed revenue of 190.49 million dollars, up 18.51 percent year over year and beating estimates by 1.11 million dollars. Earnings per share matched expectations at 0.47 dollars. Management cited portfolio expansion, active leasing, and a robust acquisition pipeline as the main drivers behind continued adjusted funds from operations growth.

The company targets high-quality retail locations that align with evolving consumer habits. Its nationwide footprint reduces regional risks and supports steady occupancy. Development backlog and disciplined capital deployment position it for further external growth in 2026. Dividend increases build on a reliable payout history suited to income investors.

Higher interest rates raise costs for new acquisitions and may pressure certain retail tenants. Yet the triple-net structure limits direct impact on cash flows and keeps distributions stable. This balance of opportunity and protection makes the name stand out for yield-focused portfolios.

We increased our position in this stock as part of the Best Monthly Dividend Stocks Portfolio. The move aligns with the portfolio mandate for attractive monthly yields backed by resilient real estate cash flows. It enhances overall income generation while adding defensive qualities in the current environment.