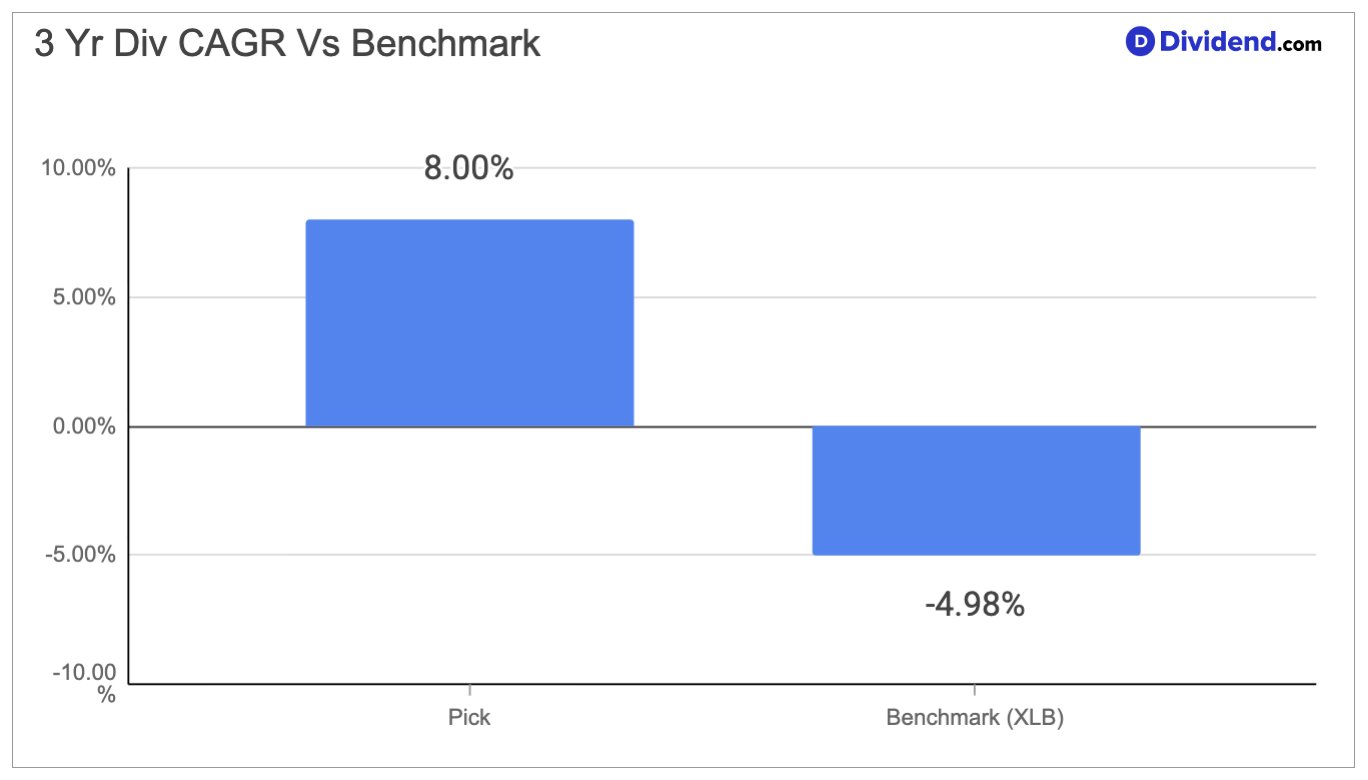

North America’s largest metals service center operator has built a compelling dividend profile that income investors rarely find in the materials sector. With a beta of 0.88, the stock moves largely in line with the broader market while offering meaningfully lower volatility than its iron and steel peers, whose average beta stands at 1.23. That reduced price sensitivity, combined with a 3-year dividend compound annual growth rate of 8%, places this company in an attractive position for investors who prize income stability alongside dividend expansion. The 8% three-year dividend CAGR ranks in the top 40% of all dividend-paying stocks, comfortably outpacing the iron and steel industry average of 2%, and signals a management team that has consistently returned more cash to shareholders year after year.

This company distributes approximately 100,000 metal products — spanning carbon steel, stainless steel, aluminum, titanium, copper, brass, and specialty alloys — to roughly 125,000 customers across industries as diverse as aerospace, defense, automotive, construction, energy, and semiconductors. Its processing capabilities, which include cutting, sawing, shearing, and blanking, are performed close to the customer at more than 300 service center locations, enabling rapid fulfillment of small-to-mid-size orders. That breadth of end-market exposure is not an accident; it is the backbone of the company’s risk management approach, designed to prevent any single industry downturn from materially disrupting revenue. The business recorded a record 6.4 million tons of metal sold in 2025, outperforming the broader metals distribution industry by more than 7 percentage points on volume growth, which demonstrates the competitive advantages embedded in its distribution network and supplier relationships.

The reaffirmation of this stock in the Best Material Dividend Stocks Portfolio reflects the enduring quality of its dividend profile and the resilience of its business model. As a holding in the Material Dividend portfolio, its combination of a well-covered payout, conservative leverage, and consistent dividend growth aligns precisely with the mandate of identifying stocks that deliver reliable, compounding income without taking on excessive risk.