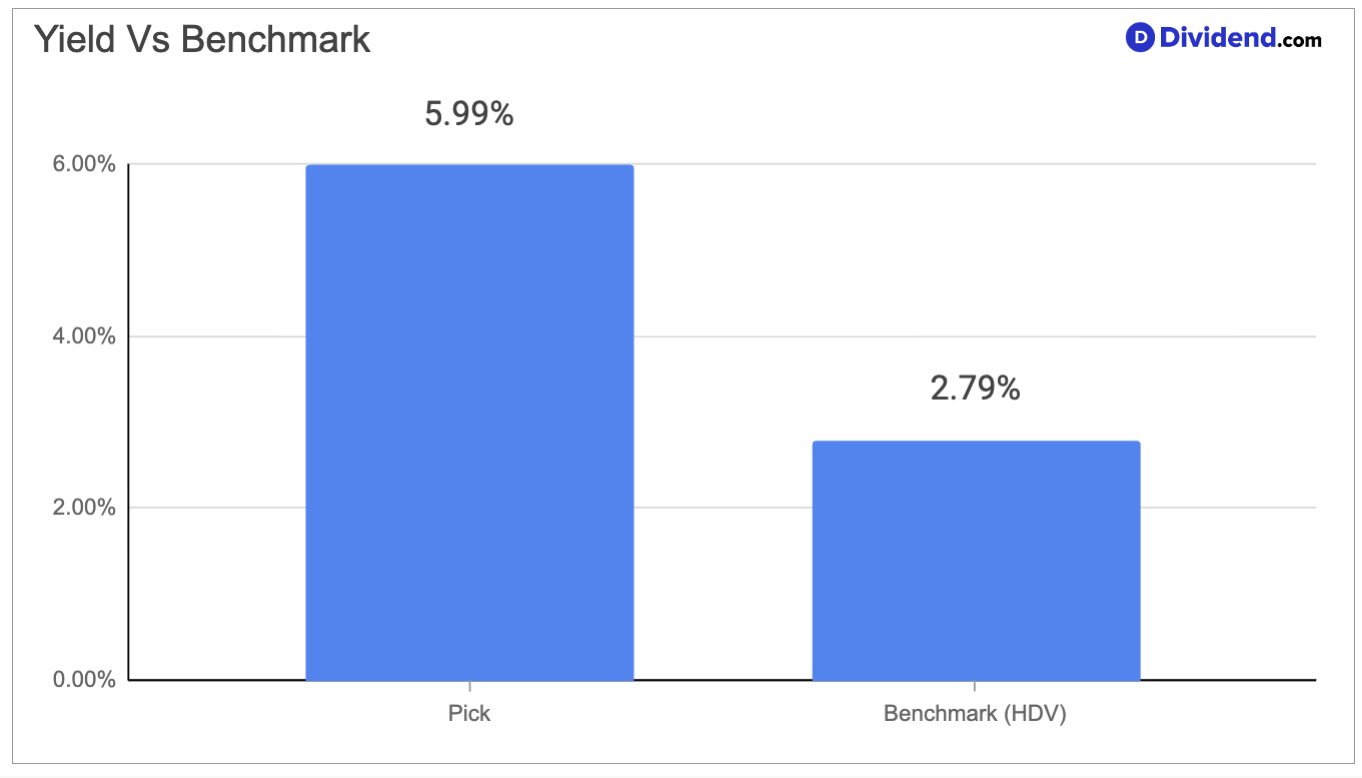

A midstream energy partnership operating one of North America’s most extensive integrated pipeline, fractionation, and export networks has earned an increased position in the Best High Yield Stocks Portfolio. With a forward dividend yield of nearly 6% and a 20+ year consecutive track record of distribution increases, this master limited partnership stands out in the Energy MLP sector as a rare combination of generous income and durable payout reliability.

Its infrastructure spans gathering, processing, transportation, storage, and export of natural gas, natural gas liquids, crude oil, petrochemicals, and refined products — serving producers, refiners, and petrochemical companies across the continental United States. The partnership’s fee-based business model insulates cash flows from commodity price swings, and its dominant Gulf Coast fractionation and export footprint positions it to capture rising global demand for U.S. energy. Its 2025 results delivered ten operational records, including record natural gas processing volumes and record NGL fractionation, underscoring the strength of its underlying infrastructure.

The partnership has also been investing heavily in its future, bringing several large capital projects online during 2025 — including a new NGL pipeline connecting Permian Basin processing plants to Gulf Coast fractionation. These investments are designed to grow NGL export capacity to approximately 1.5 million barrels per day by 2027, a trajectory directly aligned with rising international demand for cost-competitive American energy.

The near-term outlook is supported by rising natural gas demand from AI data center build-outs, utility expansion, and liquefied natural gas export terminals — all of which create incremental volume for this partnership’s integrated midstream system. Real headwinds exist, however, including lower crude oil prices compared to 2024, narrowing gas price differentials around key West Texas hubs, softer downstream product margins in areas like polypropylene, and a large legacy LPG export contract recontracted at current market rates. Management has acknowledged these dynamics while noting that the partnership’s diversified asset base allows it to benefit from price volatility on both sides of the market. The overall investment case for this partnership rests on a business that is operationally excellent, financially disciplined, and structurally positioned to grow distributions for years to come.

Increasing the position in the Best High Yield Stocks Portfolio reflects the portfolio’s mandate to own high-quality, income-generating businesses with durable cash flows and sustainable, growing payouts — exactly the profile this partnership continues to deliver.