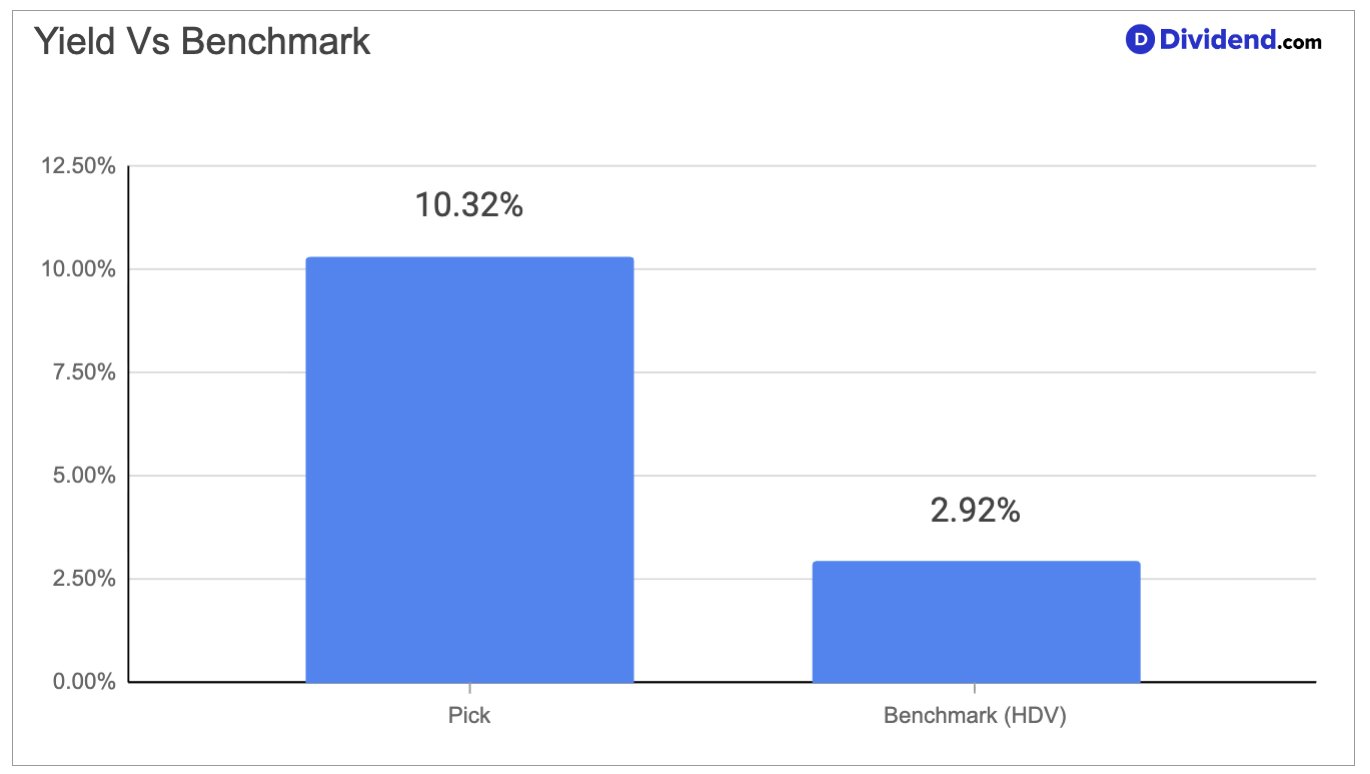

This specialty finance company operates at the heart of America’s private credit market, extending direct loans to mid-sized private businesses that fall between the reach of traditional banks and public debt markets — a structural gap that has expanded rapidly as rising borrowing costs and tightening bank regulation have pushed more companies toward private lenders. With a forward dividend yield of 10.32%, anchored by a quarterly payout of $0.48 per share, this is a company built around generating reliable, high-level income from a diversified portfolio of floating-rate loans, and its track record of sustaining that income through more than sixteen consecutive years of uninterrupted dividend payments speaks directly to the discipline embedded in how it operates. The business spans more than 600 borrower relationships across healthcare, software, business services, and financial services, giving it a breadth of exposure that reduces concentration risk while capturing income from some of the most active private equity-backed segments of the economy.

The investment case here is fundamentally about income durability, backed by scale and underwriting consistency. The company set a new annual record for loan commitments in 2025, deploying $15.8 billion in capital, while adding more than 100 new borrowers — also a company record — expanding the pipeline of future repeat-lending opportunities. These numbers reflect both the trust borrowers place in a long-standing lending relationship and the company’s growing share of what is increasingly a market for large, credentialed lenders. Growth drivers are structural, rooted in private equity deal-making activity and the preference of private businesses to consolidate borrowing with fewer, larger partners.

Key risks center on rate sensitivity — most loans earn floating-rate interest, meaning that when benchmark rates fall, investment income compresses — and on the software sector, which represents the largest single industry concentration in the portfolio. Management has acknowledged both risks openly, pointing to a $988 million spillover income cushion (approximately $1.38 per share) as a buffer that supports the dividend even when quarterly earnings dip below the payout level.

Increasing the position in this stock within the Best High Dividend Stocks Portfolio reflects the portfolio’s mandate to prioritize high, sustainable income from market-leading businesses operating in structurally growing sectors.