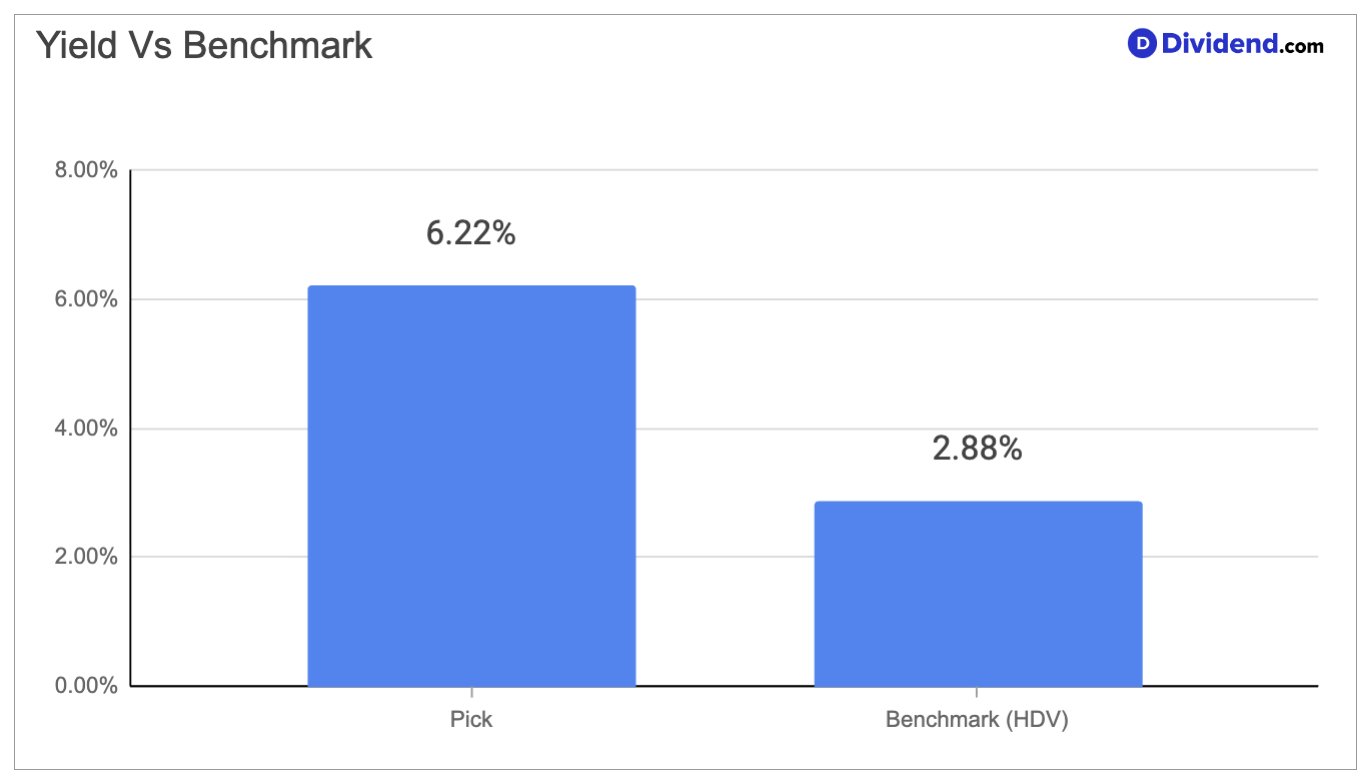

Among real estate investment trusts that focus on entertainment and hospitality destinations, few have demonstrated the combination of income reliability and external growth momentum that this large-cap experiential REIT currently offers. With a 6.22% forward dividend yield that ranks in the top 40% of all dividend-paying stocks, and comfortably above the 5.5% average for its peer group, the income proposition here is not incidental — it is structural. The company owns one of the largest portfolios of gaming, hospitality, and entertainment real estate in the United States, leased under triple-net arrangements that push property-related costs onto tenants, resulting in predictable and expense-light cash flows that form a reliable foundation for sustained dividend payments. What makes the yield especially compelling is that it has grown every single year since the company went public in 2018, compounding at roughly 7% annually — a track record that speaks to management’s confidence in the underlying cash flow engine.

The business model is built around long-term leases with some of the most durable operators in consumer entertainment, maintaining a 100% occupancy rate across the entire portfolio. This tenant quality is a critical reason why cash flows remain consistent regardless of short-term economic cycles. Beyond its core gaming real estate holdings, the company has been actively diversifying into broader experiential categories — wellness retreats, indoor waterparks, youth sports facilities, bowling and entertainment venues, and luxury real estate development — adding new income streams that reduce concentration risk while preserving the triple-net lease discipline. The first quarter of 2026 was particularly notable, as the company announced approximately $1.2 billion in new capital commitments, making it the second consecutive quarter in which new commitments exceeded $1 billion, a milestone that has never occurred before in its history. Adjusted funds from operations per share grew 4.5% year-over-year, while the share count increased by only about 1%, reflecting a disciplined approach to equity issuance that protects existing shareholders. With approximately $650 million in annual free cash flow available for redeployment and total liquidity of around $3.1 billion, the platform is positioned for continued growth without needing to dilute shareholders aggressively.

The risks are real but manageable. Las Vegas, where the company holds its most prominent and largest assets, may be entering a normalization phase after several years of exceptional post-pandemic demand, and macroeconomic uncertainty could slow the pace of new deal activity. Nonetheless, the quality of the lease structures and the financial strength of the tenant base provide meaningful insulation. For investors who prioritize compounding income from real assets with a demonstrated commitment to dividend growth, this experiential REIT presents a case that is difficult to overlook.

The decision to increase the position in the Best High Dividend Stocks Portfolio reflects the conviction that a combination of high current yield, disciplined capital growth, and conservative balance sheet management meets the portfolio’s mandate for sustainable, high-quality income generation.