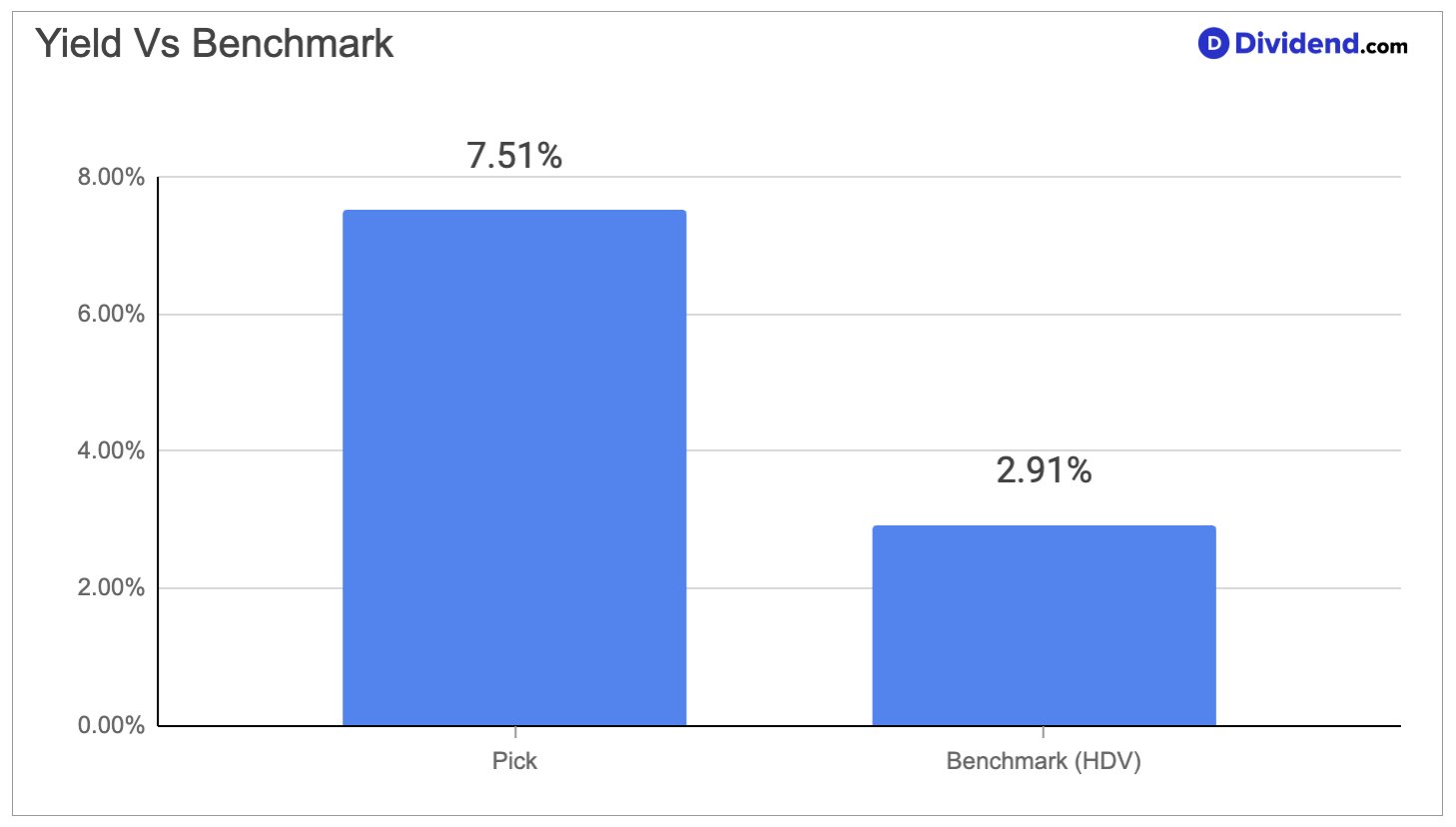

A gaming-focused net-lease real estate investment trust is delivering a forward dividend yield of 7.51%, placing it firmly in the top 20% of all dividend-paying stocks. That yield is not a product of distress or financial strain — it is the direct result of a business model built around collecting rent from some of the largest regional casino operators in the country, under long-term leases that require tenants to cover property taxes, insurance, and maintenance. This structure keeps the company’s cash flows predictable and insulated from the ups and downs of gaming revenues, since the rent arrives regardless of how the casino floor performs on any given quarter. With more than 65 properties leased across roughly 20 states, the portfolio is broadly diversified across geographies and tenants, which further anchors the income stream underlying this yield.

The company has also built a meaningful growth engine on top of its rent-collecting foundation. A pipeline of nearly $2 billion in committed future capital deployments, targeted through year-end 2027, is set to drive incremental AFFO per share higher over the coming years. Acquisitions completed in recent quarters — including major gaming facilities in key metropolitan markets — have already contributed tens of millions in additional annual cash rent, and further transactions are expected to close in the near term. The company does carry a meaningful debt load relative to its asset base, which is not unusual for net-lease REITs of this scale, and management has kept leverage at the lower end of its stated target range. Development concentration in a small number of large projects represents a risk worth monitoring, but management has placed exposure caps on individual transactions to limit the impact of any single project.

Increasing our position in this gaming and entertainment REIT in the Best High Dividend Stocks Portfolio reflects the portfolio’s commitment to sustainable, above-average income supported by predictable, contractually secured cash flows. The combination of a top-tier yield, a growing capital deployment runway, and a business model insulated from operational volatility makes this an especially well-suited holding for income-focused investors.