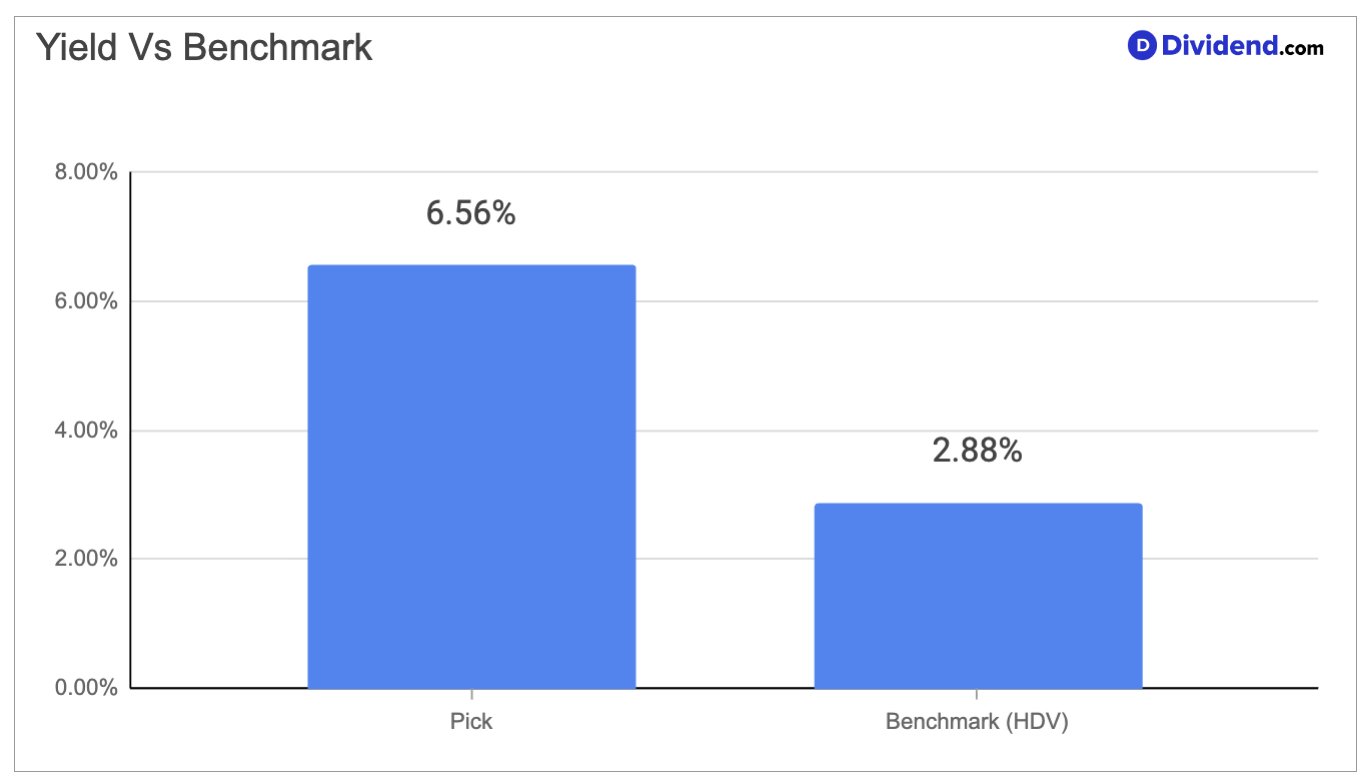

A self-managed real estate investment trust focused entirely on gaming and entertainment properties is generating one of the more compelling income profiles in the broader REIT universe. With a 6.56% forward dividend yield ranking in the top 40% of all dividend-paying stocks, this Pennsylvania-based company has built a model that converts long-term, triple-net leases on casinos, racinos, and regional entertainment venues into a steady, predictable stream of rental income. Rather than operating gaming facilities itself, the company structures its leases so that tenants absorb property taxes, insurance, and maintenance costs, creating a lean ownership model that channels the bulk of revenue toward distributions and reinvestment. In its Q1 2026 earnings call, management reported mid-to-high single-digit growth in adjusted funds from operations per share, and described early 2026 tenant performance as notably encouraging after a soft patch in 2025.

What makes this income stream particularly durable is the nature of the underlying real estate. Gaming facilities are deeply embedded in their local economies, serve as anchor assets for regional tourism and entertainment, and are difficult to relocate or replicate. The company has assembled a geographically diversified portfolio of more than 65 properties across roughly 20 states, and it continues to expand through disciplined sale-leaseback transactions and development commitments.

The company does carry meaningful debt, and large development commitments introduce some execution uncertainty over the medium term, with management citing absolute exposure caps on its largest individual projects. However, the leverage ratio stood at 5 times net debt to EBITDA at the end of Q1 2026, at the low end of the company’s own targeted range, and management expressed confidence in sustaining leverage within a 5.0 to 5.5 times band even after further capital deployment. Full-year 2026 adjusted funds from operations guidance was set at $1.212 billion to $1.223 billion, or $4.08 to $4.12 per diluted share, with outstanding future capital commitments of roughly $1.8 billion targeted for deployment by year-end 2027.

This is precisely the kind of income-oriented real estate holding that fits the mandate of the Best High Dividend Stocks Portfolio. The combination of a top-decile yield, long-term lease structures, a stabilizing tenant base, and a visible pipeline of earnings-accretive capital deployments makes it a well-rounded addition for investors focused on sustainable high income. We increased our position in this holding because its yield strength, disciplined leverage management, and expanding asset base align directly with our approach to selecting durable, high-yield dividend stocks.