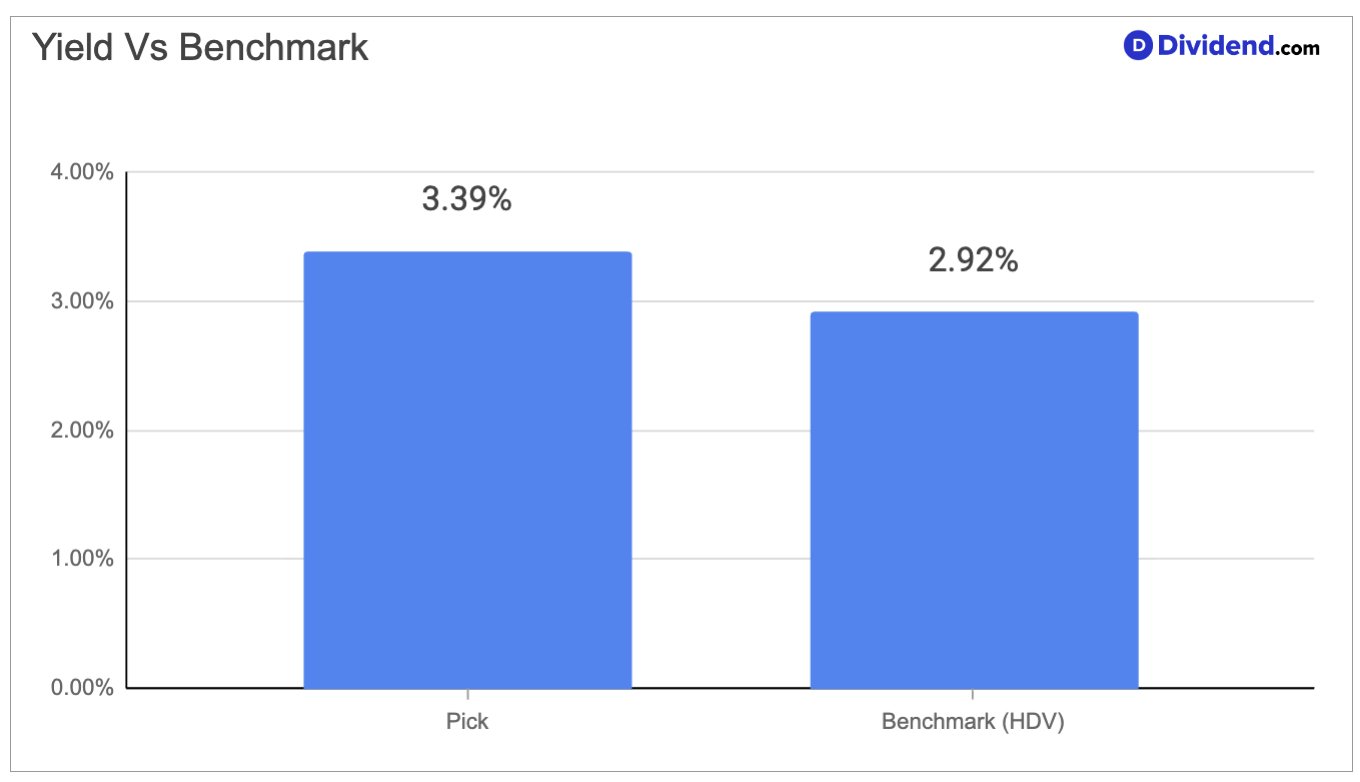

Among the largest electricity and natural gas distributors in the United States, this Southeast- and Midwest-anchored utility has quietly built one of the most durable dividend track records in its sector — 21 consecutive years of dividend increases — while now deploying what it describes as the largest capital investment plan in the U.S. utility industry. At a forward yield of 3.39%, the stock sits near the middle of all dividend-paying equities, but what makes it noteworthy for high-income investors is not just the yield in isolation; it is the combination of a well-covered payout, steady earnings growth, and a business model built around regulated, essential-service revenues that tend to hold up regardless of broader economic conditions.

The company operates across two primary business lines — electric utilities and natural gas infrastructure — serving residential, commercial, industrial, and wholesale customers across six states. Its growth strategy is increasingly shaped by the surging demand for data center power, electrification of transportation, and renewable energy integration, all of which are expected to drive sustained volume growth over the coming decade. At the same time, the business faces real headwinds, including elevated debt from its ambitious capital program, the recurring financial burden of storm recovery costs, and the ongoing challenge of keeping customer bills affordable while simultaneously funding major infrastructure upgrades.

These tensions between growth ambition and financial discipline are central to understanding how this utility fits within a high-yield income strategy — and why a careful assessment of yield, safety, and return potential is essential before sizing any position. We have increased our position in this stock within the Best High Yield Stocks Portfolio, reflecting confidence in its capacity to deliver reliable, growing income alongside measured capital appreciation for long-term dividend investors.