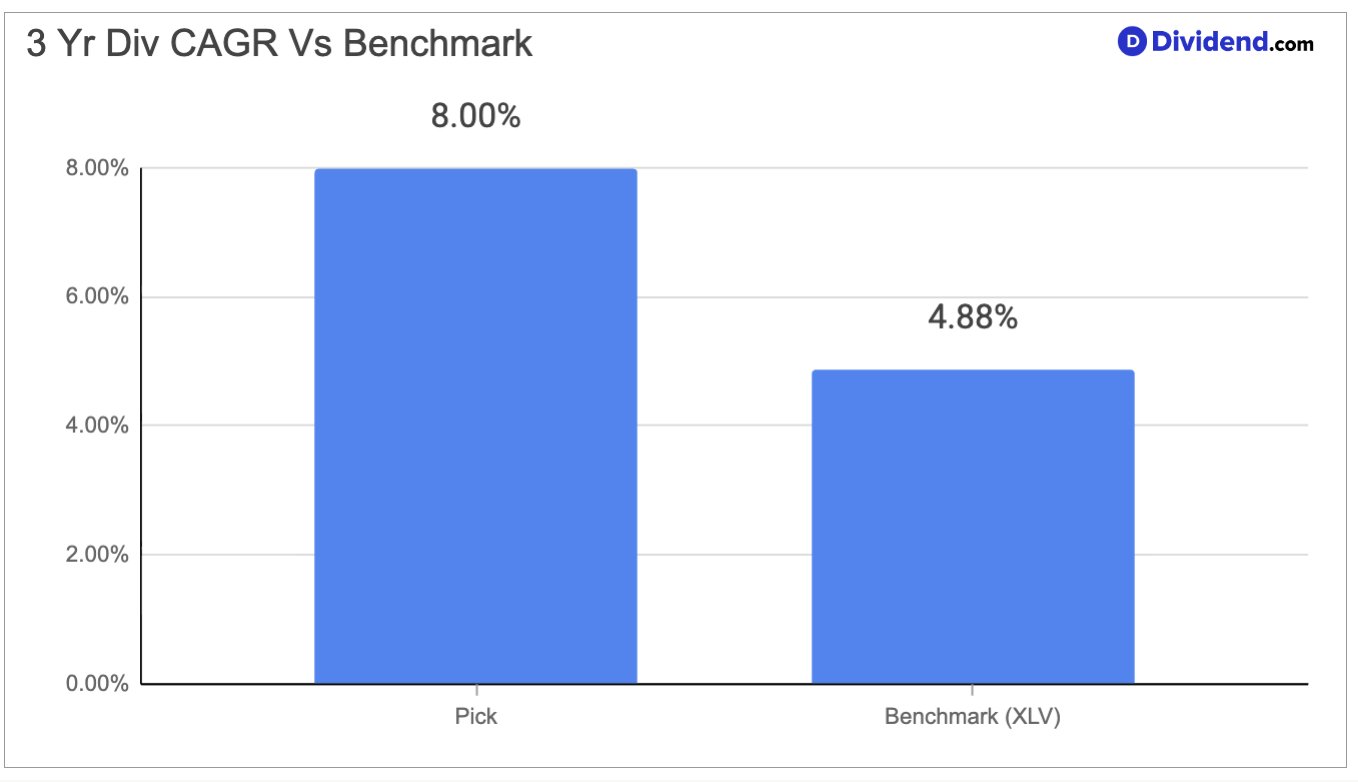

A diversified health services company sits at the intersection of pharmacy benefit management and health insurance, giving it a unique vantage point over drug spending and patient outcomes. Its stock carries a beta of 0.30, meaning its monthly price swings show little correlation with the broader equity market, a trait that appeals to investors seeking steady exposure. Dividend growth has also been healthy, with the dividend per share compounding at an 8% annual rate over the past three years, a pace that outpaces many peers in its industry group. The company pairs this growth with a payout ratio that remains comfortably low, leaving ample room for future increases even as it navigates a significant transformation of its core pharmacy benefit business.

The company operates through two complementary segments, one focused on specialty pharmacy and pharmacy benefit services and the other on employer-sponsored and individual health coverage. Recent growth has been driven by accelerating demand for specialty drugs and biosimilar medicines, alongside a health insurance segment benefiting from favorable medical cost trends. At the same time, the business is in the middle of restructuring its pharmacy pricing model, a shift that management expects will strengthen its long-term competitive position even though it creates near-term earnings pressure. These crosscurrents, growth in specialty and insurance operations set against a multi-year pricing transition, are the same dynamics reviewed carefully within our income-focused research.

This stock’s blend of low volatility, above-average dividend growth, and improving core operations supports its continued place among reaffirmed holdings in the Best Health Care Dividend Stocks Portfolio. The mandate favors companies capable of generating durable income while limiting downside risk, and this business reflects both qualities. Its ongoing transformation adds complexity worth monitoring, but current fundamentals justify keeping the position intact.