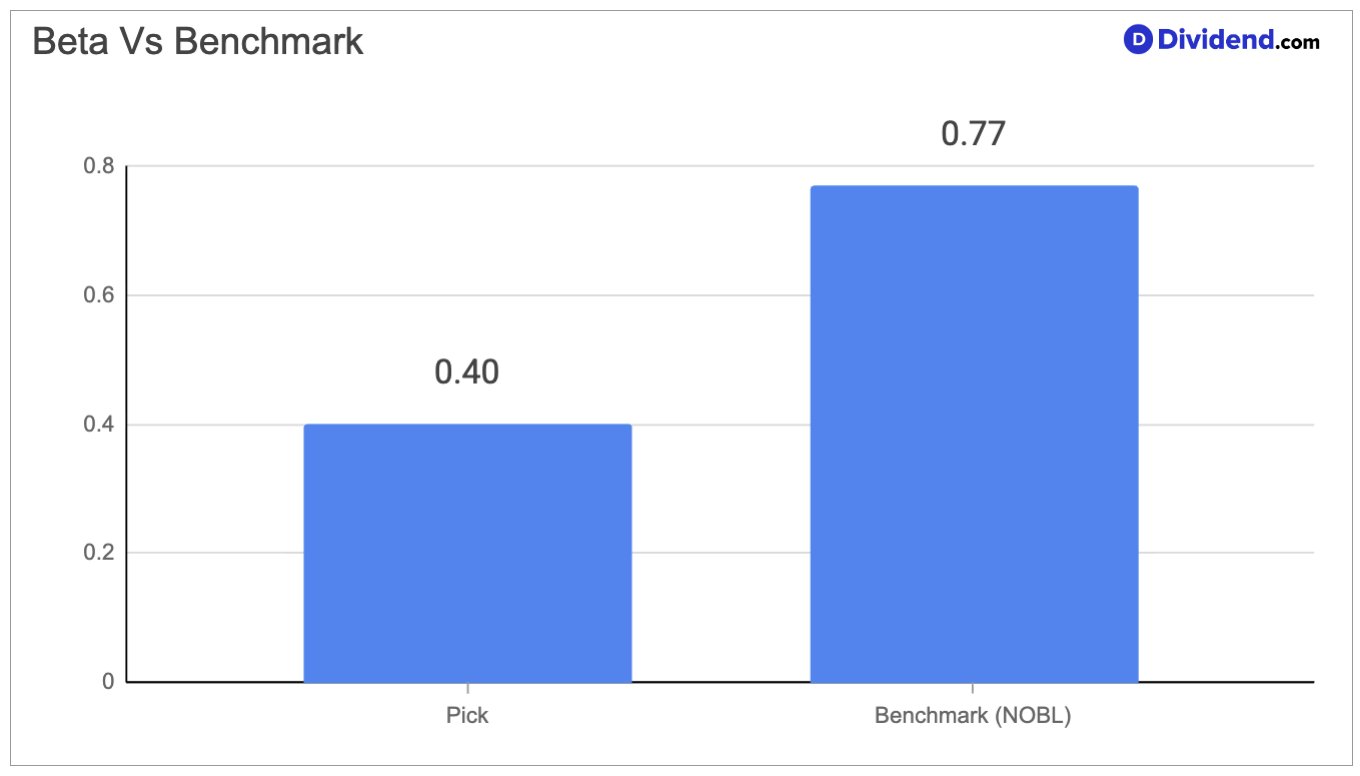

A global consumer staples company specializing in biscuits, baked snacks, chocolate, and confectionery — selling to consumers across more than 150 countries — has earned an increased position in the Best Dividend Stocks Portfolio. The business has raised its dividend for 14 consecutive years, and its 3-year dividend compound annual growth rate of 7% ranks in the top 40% of all dividend-paying stocks, well above the Consumer Products industry average of 4%. With a beta of just 0.40, the stock has demonstrated exceptionally low sensitivity to broad market movements over the past 5 years, making it one of the more stable price performers in the consumer staples space. The company operates two core revenue pillars — biscuits and baked snacks on one side, and chocolate and candy on the other — generating the majority of its sales outside the United States, with emerging markets in Asia, Latin America, and developing economies accounting for approximately 40% of total revenue.

The near-term picture carries some complexity. Cocoa commodity costs created meaningful margin pressure through much of 2025, and while the situation has improved materially — with industry coverage now exceeding 10 months of forward pricing — the elevated payout ratio of 64% is a factor that deserves attention. That ratio sits above the 50% Consumer Products peer average, meaning the dividend consumes a larger share of earnings than is typical for the group, leaving somewhat less buffer in a stress scenario. Yet the business is also forecast to grow earnings per share by 11% in the coming fiscal year, outpacing the 7% peer average, and emerging market revenue growth of 6.3% in the first quarter of 2026 signals that the company’s international footprint is delivering volume-driven expansion, not just price increases.

This increased position in the Best Dividend Stocks Portfolio reflects the portfolio’s recognition that the company’s long track record of dividend growth, low-volatility price behavior, and durable global brand presence form a compelling income foundation for quality-focused investors. The decision to add to this holding at current levels reflects a view that the near-term headwinds are transitional, while the structural income and growth characteristics of the business remain firmly intact.