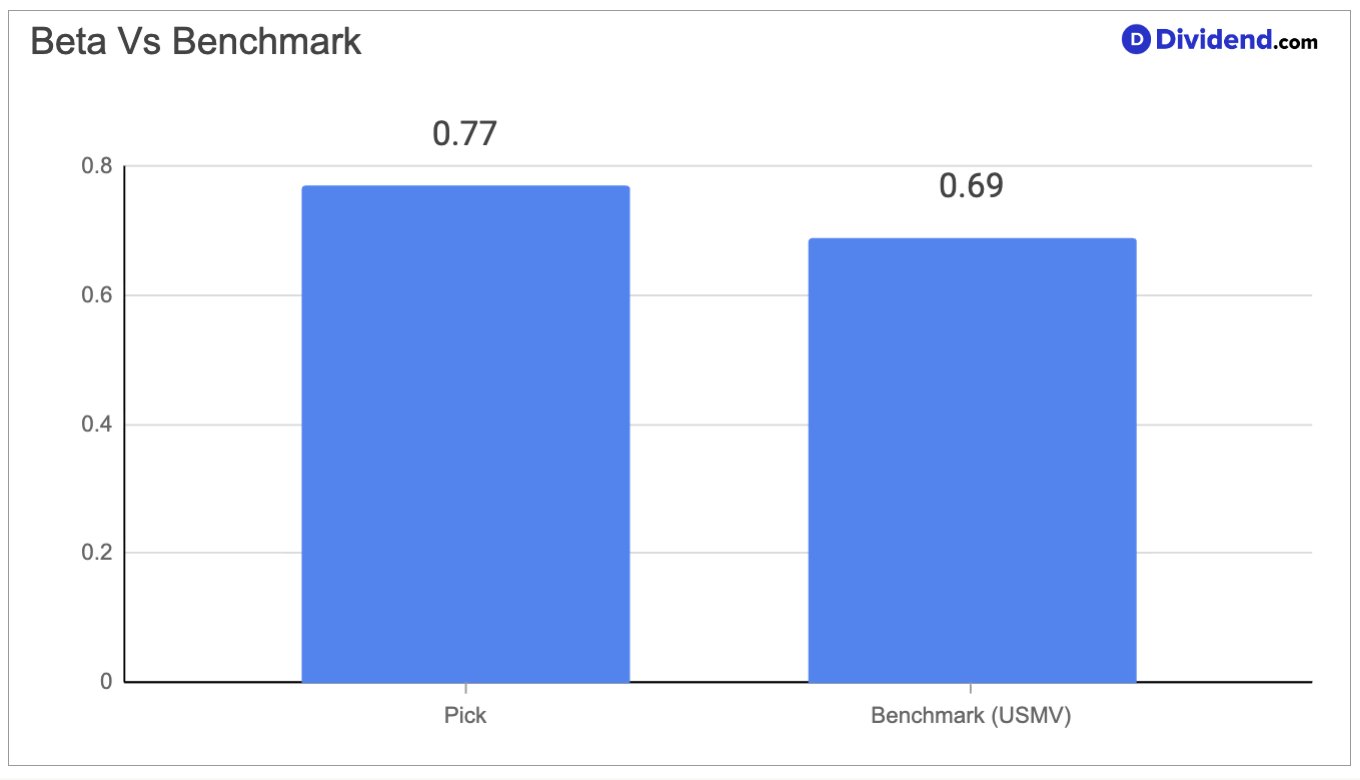

This is a large-cap, S&P 500-listed residential rental real estate investment trust with a portfolio spanning more than 100,000 apartment homes across the Sun Belt — a region of the United States defined by strong population inflows, job market expansion, and housing costs that remain more affordable than the major coastal metros. The company’s beta of 0.77 signals that its stock price moves with meaningfully less sensitivity to broader equity market swings than the average stock, making it a natural fit for income investors who prioritize capital stability alongside yield. The business is at a transitional moment, navigating the final stages of an elevated apartment supply cycle while simultaneously laying the groundwork for a return to stronger rental pricing as new construction activity decelerates sharply.

The operating environment for Sun Belt apartment landlords has been testing over the past two years, with a wave of newly delivered apartment units pressuring occupancy and rental rate growth in several key markets. That tide, however, appears to be turning. New apartment deliveries are expected to decline more than 60% from their cycle peak in 2026, while new construction starts have been depressed for nearly three years and currently sit roughly 70% below their own peak. This structural shift in supply is the single most important forward-looking development for the business, and management has guided for meaningful improvement in blended lease rate growth and effective rent growth over the coming year relative to 2025.

The company’s operating platform is technology-forward, with community-wide Wi-Fi rollouts and unit renovation programs set to accelerate in 2026, both of which support resident retention and justify higher rents over time. Resident turnover has remained at historically low levels — a reflection not only of operational quality but of the structural affordability challenge in the single-family housing market, where elevated mortgage rates have extended rental tenure for many would-be homebuyers. That dynamic has been an underappreciated demand stabilizer for the business. Meanwhile, a strong balance sheet with nearly $880 million of combined cash and borrowing capacity gives management genuine flexibility to pursue opportunistic acquisitions and new developments as the recovery gains momentum.

The reaffirmation of this stock in the Dividend Protection Stocks Portfolio reflects the portfolio’s mandate of identifying income-generating equities where the dividend is structurally protected, downside risk is bounded, and the business model is built for durability through different parts of the economic cycle. A 17-year consecutive dividend increase track record, a market-cap that sits well above the peer group average, and a low-beta profile together form the foundation of this reaffirmation — and the following analysis explains precisely why those characteristics hold up under scrutiny.