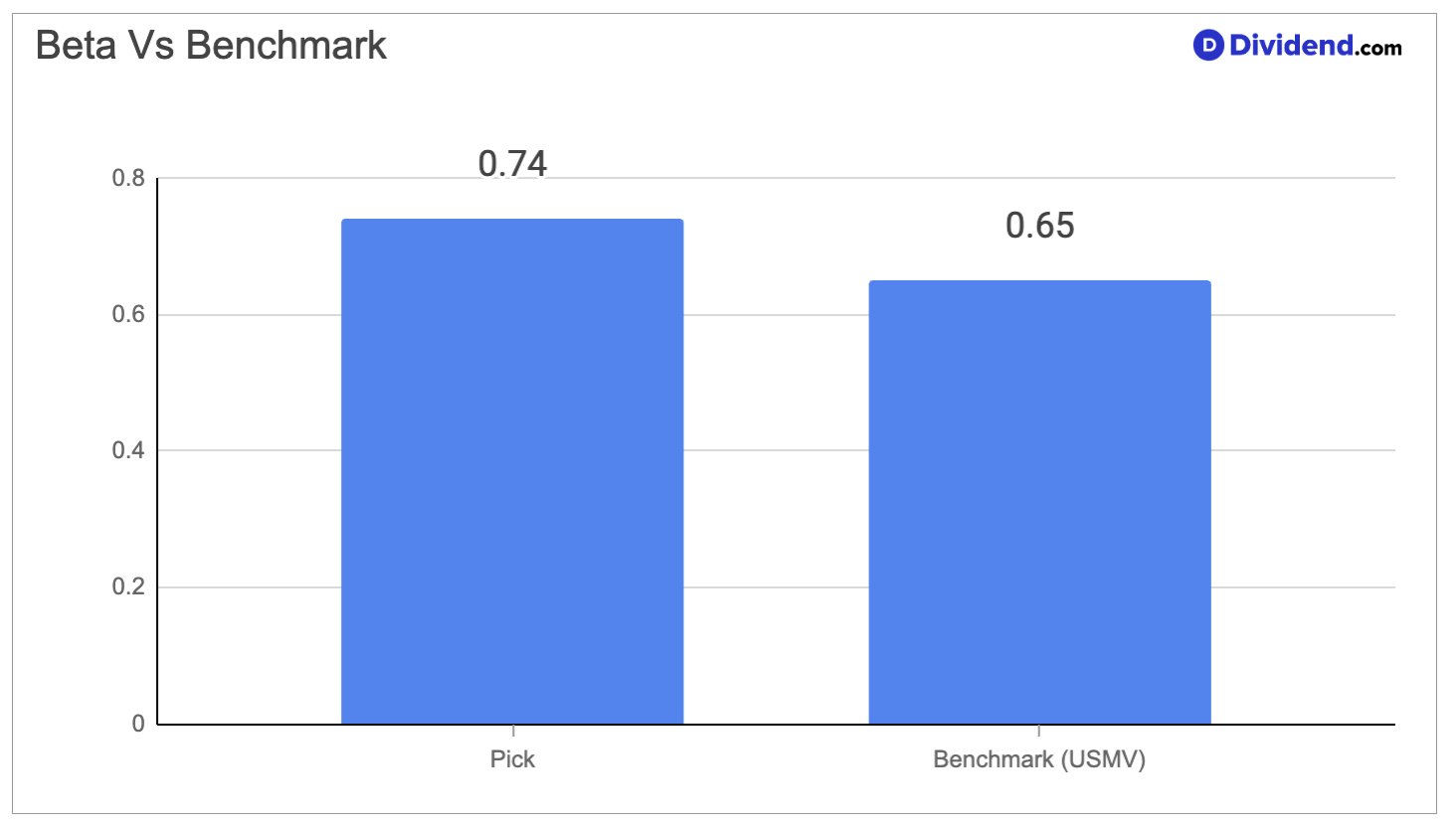

A large-cap residential REIT operating exclusively across the high-growth Sun Belt and Southeast United States has earned an increased allocation in the Dividend Protection Stocks Portfolio, and the reasons run deeper than yield alone. This is a company that owns, operates, and develops multifamily apartment communities — spanning garden-style, mid-rise, and high-rise formats — in markets that continue to attract population and employment migration from more expensive coastal cities. With a beta of 0.74, the stock moves meaningfully less than the broader equity market on a month-to-month basis, which is precisely the kind of low-correlation profile that conservative income investors need when positioning for downside protection. Occupancy has held at 95.5%, and management reported a meaningful earnings beat in Q1 2026, with internal value-creation programs tracking above their own targets. These are not incidental data points — they are signals of an operating model that consistently finds ways to generate cash flow even when the pricing environment is difficult.

The near-term challenge worth acknowledging is new lease pricing, which has faced pressure from a wave of new apartment supply in several Sun Belt cities. Markets like Austin, Nashville, and Atlanta saw elevated construction completions through 2024 and 2025, which kept rent growth from returning to positive territory for new leases. Management was transparent about this headwind on its most recent earnings call, while also noting that March and April showed sequential pricing improvement following a softer February. The company’s disciplined payout history — 17 consecutive years of dividend increases — reflects an ability to navigate exactly these kinds of transitory operating pressures without compromising its income commitment to shareholders. Common area repositioning projects are generating net operating income yields above 10%, and the broadband infrastructure rollout is adding ancillary revenue streams with minimal capital intensity. The supply cycle that pressured rents through 2024 and 2025 is now expected to peak and roll over in 2026, setting the stage for a meaningful recovery in pricing power across the portfolio.

Increasing this position in the Dividend Protection Stocks Portfolio reflects conviction that the company’s combination of low market sensitivity, long dividend growth track record, and improving internal operating momentum makes it well suited to anchor an income-focused, risk-aware allocation. As the Sun Belt supply cycle turns, this REIT is positioned to be one of the clearer beneficiaries among residential property owners — and its defensive financial profile makes it an appropriate fit for investors whose priority is protecting the dividend above all else.