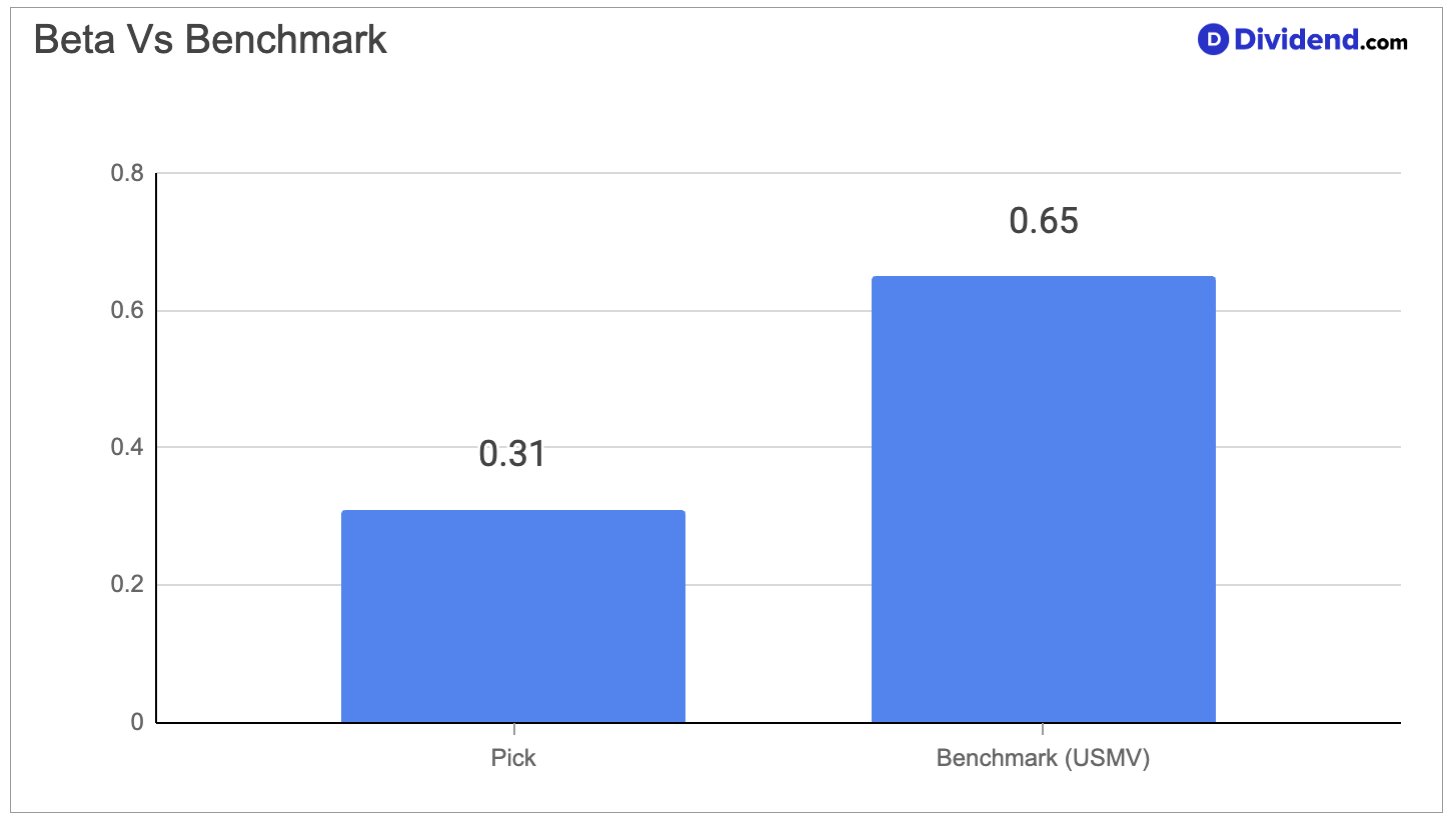

A global biopharmaceutical company operating in immunology, oncology, neuroscience, and aesthetics has quietly become one of the most compelling dividend stories in large-cap health care. The company has raised its dividend for more than 50 consecutive years, a streak that places it among a very small group of companies worldwide with that level of payout discipline. Its beta of 0.31 means that its stock price moves very little relative to the broader equity market, making it an unusually stable holding for income-focused investors who cannot afford sharp portfolio swings. Over the past several years, the company executed one of the most difficult transitions in pharmaceutical history — replacing a blockbuster drug that once generated over $20 billion annually after generic competition eroded its exclusivity — and it did so while continuing to grow its revenue, raise its dividend, and expand its pipeline. That combination of operational resilience and shareholder commitment forms the backbone of the investment case here.

The company’s two lead immunology treatments — a biologic therapy targeting multiple inflammatory conditions including a debilitating skin disease and an oral medicine approved across a wide range of autoimmune disorders — have now grown large enough together to surpass what the former flagship drug contributed at its peak. The immunology franchise generated more than $7 billion in revenue in a single quarter, a figure that underscores how completely the product transition has been executed. Beyond immunology, the neuroscience segment delivered 24% growth, and the aesthetics business — centered on cosmetic treatments and injectable fillers — returned to growth after a period of softness driven by slower consumer demand in one international market. This is a business that is growing while paying a generous, well-covered dividend, and it carries a payout ratio of just 47%, which leaves ample room to sustain and continue growing distributions even if near-term earnings growth moderates.

The Dividend Protection Stocks Portfolio has increased its position in this large-cap biopharmaceutical company, reflecting our increased conviction in its ability to deliver safe, growing income in a low-volatility package. The combination of an extraordinary dividend increase track record, a deeply defensive stock price profile, and a business that is demonstrably transitioning from single-product dependence to multi-franchise durability makes it a strong fit for the portfolio’s mandate of protecting capital while reliably delivering dividends.