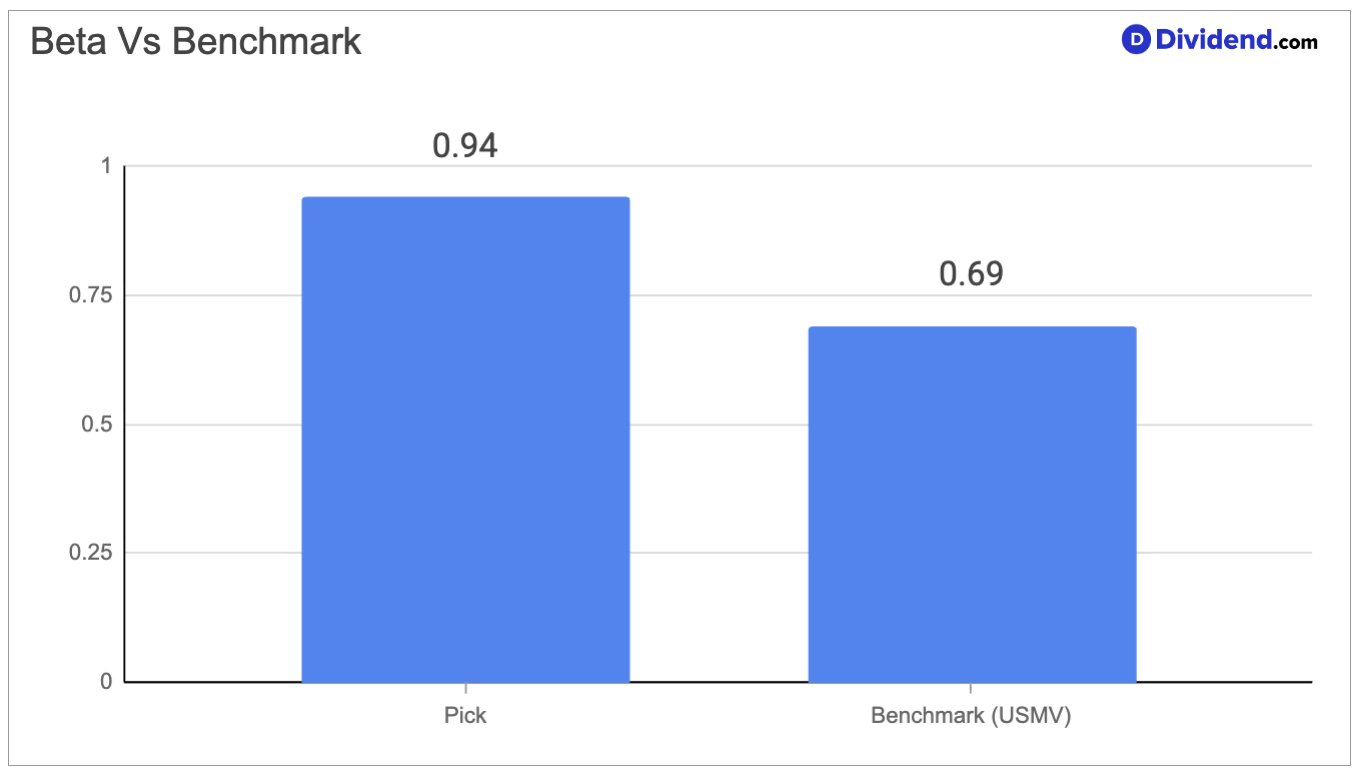

Canada’s largest bank by assets is not merely a financial institution — it is a diversified financial services platform with deep roots across personal banking, commercial lending, wealth management, insurance, and capital markets. Operating across Canada, the United States, and 27 additional countries, this institution serves over 19 million clients through an integrated model that has been refined over more than 160 years. What makes this bank particularly compelling for conservative income investors is its combination of business scale and financial discipline. Its beta of 0.94 signals that it behaves very much in line with the broader equity market, neither dramatically amplifying gains in bull markets nor catastrophically magnifying losses in downturns, which is precisely the kind of temperament suited to a dividend protection mandate. The bank operates through five distinct business lines that collectively provide meaningful revenue diversification, reducing dependence on any single economic cycle or interest rate environment.

The bank’s core growth engine has recently demonstrated notable momentum. Its wealth management and capital markets segments delivered record results in the most recently reported quarter, and the successful absorption of a major domestic acquisition has added a new layer of commercial and high-net-worth client exposure. Management has signaled a disciplined approach to future capital deployment, prioritizing organic growth and capital-light businesses over further large-scale transactions. Meanwhile, trade-related uncertainty in the Canadian economy has introduced some caution into commercial loan growth and mortgage origination, reflecting a broader macroeconomic environment that continues to evolve. The bank has acknowledged that credit losses in the near term may remain somewhat elevated, though the trajectory is expected to improve as trade conditions stabilize.

This bank’s inclusion with an increased position in the Dividend Protection Stocks Portfolio reflects a deliberate alignment with the portfolio’s mandate of prioritizing dividend safety and low return risk above all else. The institution’s 16-year consecutive dividend increase track record, net leverage profile that is well below its peer group, and a payout ratio that remains comfortably within sustainable bounds all reinforce the case for expanding this holding within a defensive income strategy.