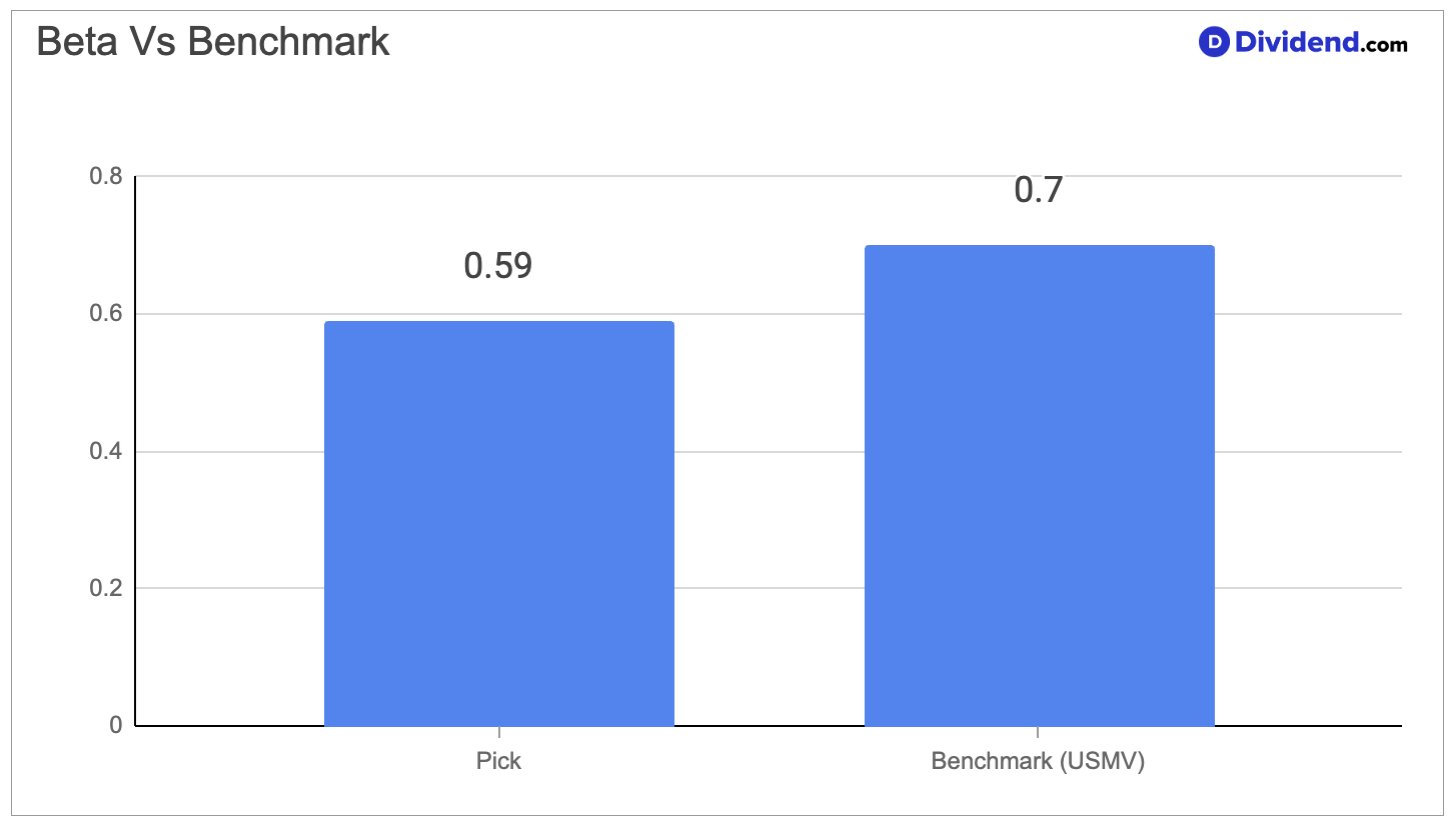

This waste services provider maintains a low beta of 0.59, which helps shield investor returns from broad market swings. Its operations focus on essential collection, transfer, and recycling services across residential, commercial, and industrial clients, ensuring steady demand even in tough economic times. Growth comes from pricing discipline, cost efficiencies, and investments in renewable energy projects, while risks like commodity price fluctuations are managed through diversified revenue streams and regulatory compliance.

The company delivers integrated environmental solutions, emphasizing sustainability and waste diversion. It benefits from long-term contracts and a vast network of facilities, which support consistent cash flows. Expansion in recycling and gas-to-energy adds revenue layers, countering challenges from integration costs or external events.

We increased our position in the Best Dividend Protection Stocks Portfolio because this stock aligns with our focus on safe, low-volatility income generators. Its resilient business model and strong financial health make it a solid anchor for conservative portfolios. This move enhances our exposure to dependable dividend payers in essential services.