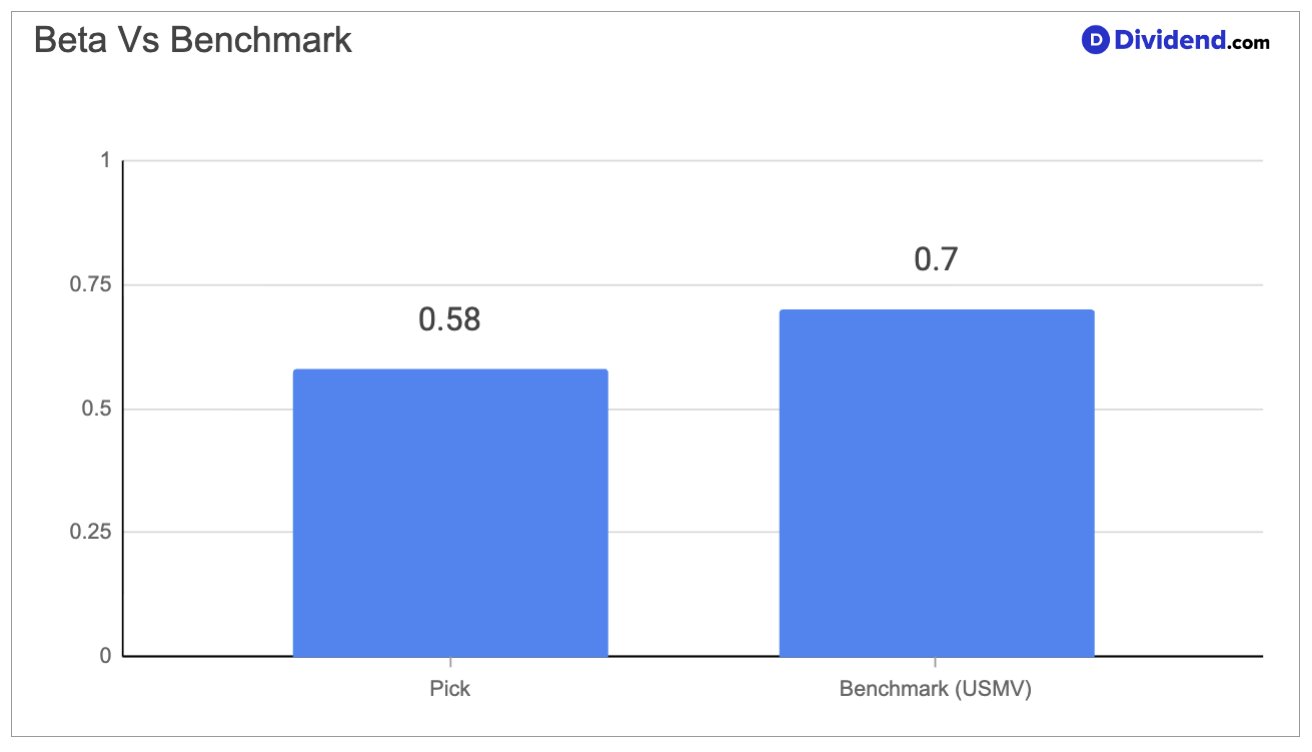

This regional bank stands out with its low 0.58 beta, which helps reduce portfolio swings during market ups and downs. It offers banking services for individuals and businesses, along with wealth management, across a focused area in the U.S. Northeast and Mid-Atlantic. Growth comes from expanding loans in commercial and consumer areas, plus rising fee income from trusts and mortgages. Risks include economic slowdowns that could affect deposits and loan quality, but strong capital levels provide a buffer.

The bank operates over 900 branches, serving a mix of small businesses, larger firms, and personal clients through deposits, loans, and financial planning tools. Its recent earnings show record net income, driven by efficient operations and automation. Loan balances grew in key segments like residential mortgages and specialty lending. Fee revenues hit new highs from mortgage banking and trust services. Management focuses on simplifying processes to boost efficiency. Headwinds involve competition for deposits and potential policy changes, yet asset quality remains solid with low nonaccrual loans.

Challenges arise from a cautious economy, but the bank’s resilient balance sheet and controlled expenses support ongoing stability. Outlook includes moderate loan and fee growth, with net interest income steady amid expected rate adjustments. This positions it well for consistent performance.

We have increased our position in the Dividend Protection Stocks Portfolio because this stock aligns with the mandate of prioritizing dividend safety and low volatility. Its strong cash flows and prudent leverage enhance reliability for income preservation. This move bolsters the portfolio’s defensive stance against market uncertainties.