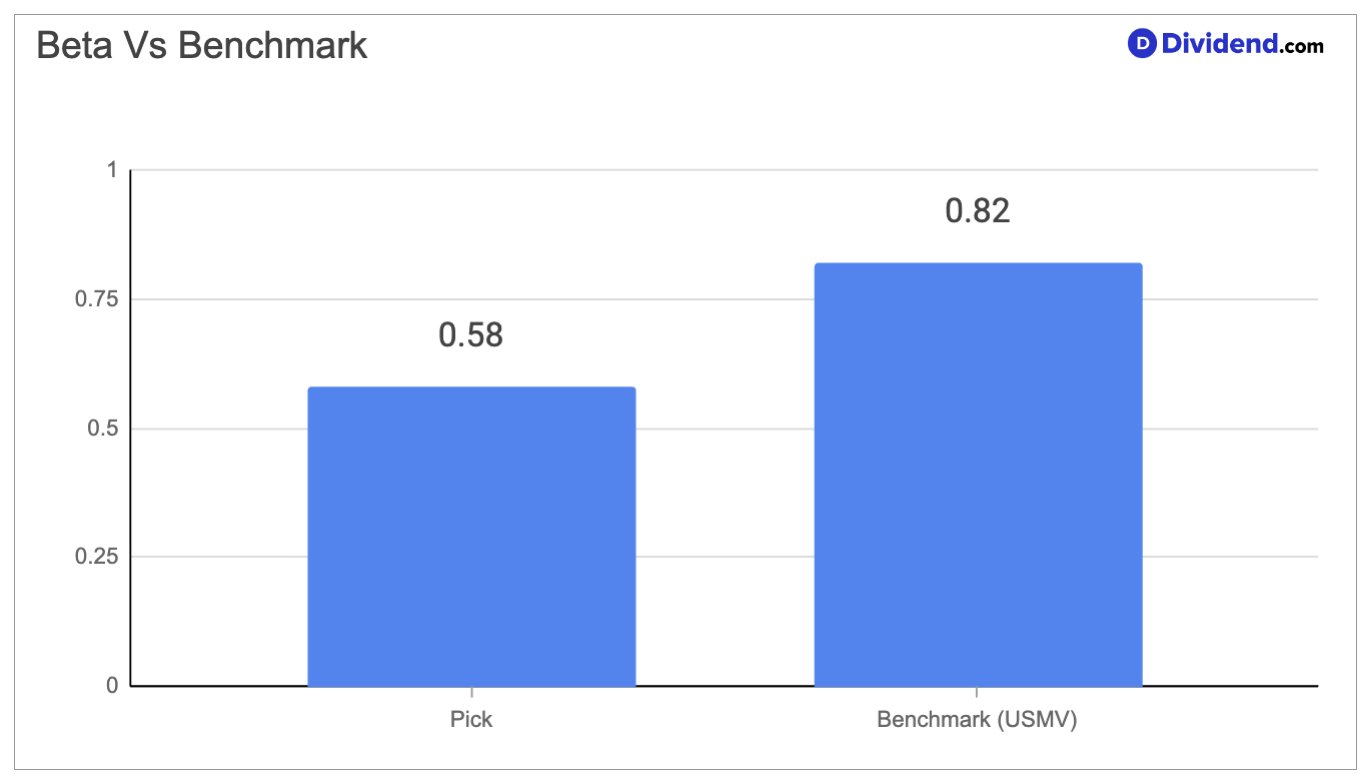

A regulated electricity and natural gas distributor serving millions of customers across one of the most economically active regions of the United States, this utility has quietly built one of the most reliable dividend track records in the integrated utilities sector. With a beta of 0.58, its share price moves at roughly half the pace of the broader equity market, making it a natural anchor for income investors who prioritize capital stability over speculative upside. The company’s regulated monopoly structure, combined with a fleet of clean, baseload nuclear generation assets, insulates revenue from the competitive pressures that weigh on many energy businesses, while its expanding infrastructure investment program signals durable, state-regulated earnings growth for years ahead.

The utility’s growth story is grounded in a multi-year capital investment cycle, backed by its regulator, that is designed to harden the grid, improve energy efficiency, and accommodate rising electricity demand from large commercial and industrial customers. Its nuclear operations ran at a 91.2% capacity factor in 2025, well above the industry norm, demonstrating operational discipline that directly supports the predictability of cash flows underpinning the dividend. At the same time, risks are present and worth acknowledging — the expiration of a state clean-energy subsidy program reduced power segment revenues in the second half of 2025, and ongoing regulatory engagement around electricity rate affordability creates a layer of political risk that investors must monitor.

This is the kind of business that the Dividend Protection Stocks Portfolio is designed to hold — regulated, cash-generative, and structurally insulated from economic cycles. We increased our position in this utility because its combination of low price volatility, a 15-year dividend growth streak, and a fully funded multi-year capital plan aligns precisely with the portfolio’s mandate of preserving income and protecting capital for risk-averse investors.