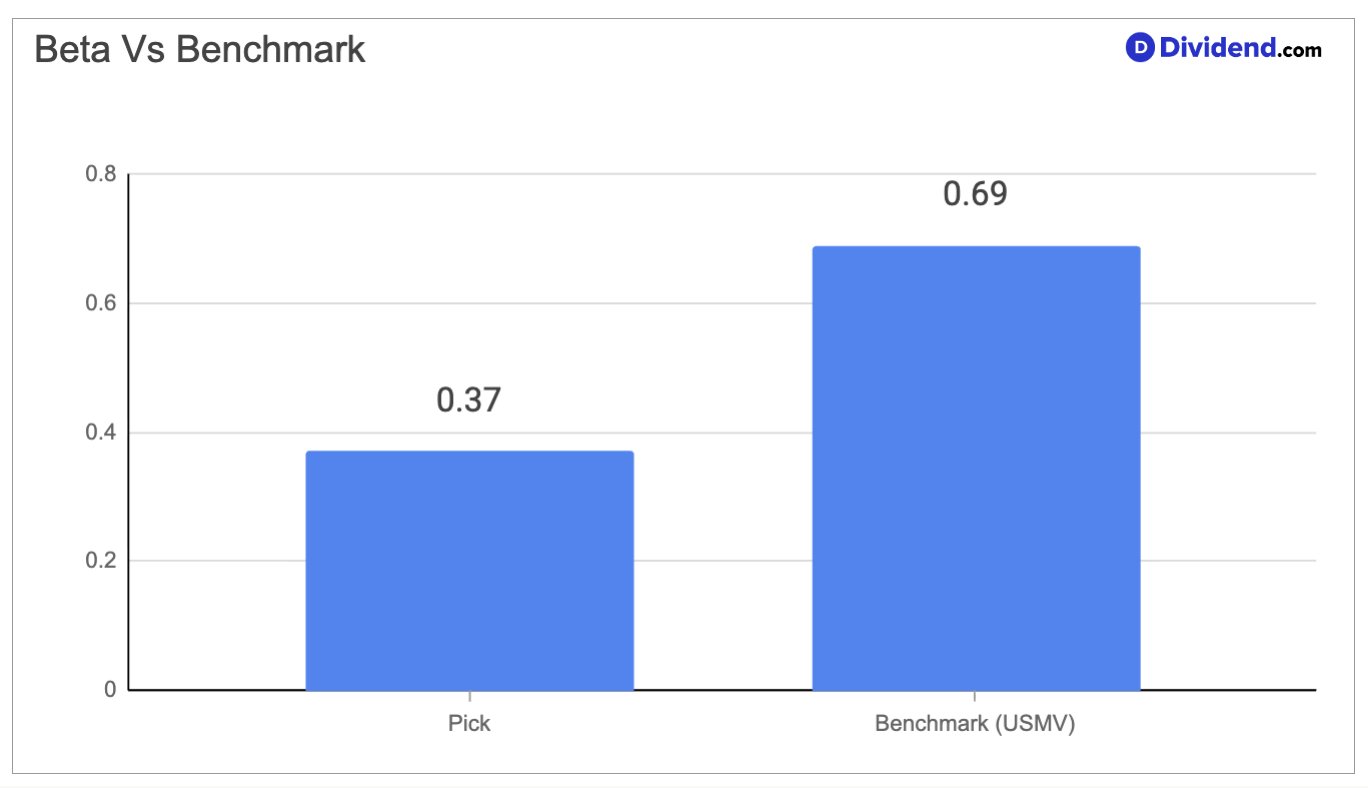

Few companies in the industrials sector can claim the combination of structural earnings durability, 35 consecutive years of dividend increases, and a price beta of just 0.37 — a figure that tells investors this stock barely moves in lockstep with the broader market, even during periods of elevated volatility. This aerospace and defense company operates across four major business lines: designing and building nuclear-powered submarines and surface combatants for the U.S. Navy, manufacturing battle-proven armored vehicles and munitions for land forces worldwide, producing large-cabin ultra-long-range business jets that command a leading share of their market, and delivering advanced technology and mission-critical intelligence services to government and defense agencies. The combination of long-cycle government contracts, a diversified revenue base spanning both military and commercial markets, and deep integration with national security infrastructure gives this company a resilience profile that few industrial businesses can match.

The business has benefited from a convergence of powerful and durable demand tailwinds. Rising global defense budgets — driven by heightened geopolitical tensions, NATO allies expanding land systems procurement, and a generational push by the U.S. Navy to modernize its undersea fleet — have driven orders that extend years into the future. At the same time, sustained corporate demand for ultra-long-range business aviation has kept the commercial side of the business robust, providing a meaningful offset to the cyclicality that often characterizes pure-play defense firms. The company closed its most recent fiscal year with a total backlog of nearly $120 billion, a 30% increase year-over-year, representing extraordinary earnings visibility for a company of this scale.

Growth has not been without its challenges. Skilled labor availability and supply chain bottlenecks have constrained how quickly submarine production can be ramped up to match swelling order books, and the technology and services segment has faced near-term headwinds from government contracting delays. There are also cost-management considerations in the aviation business related to component sourcing and tariff exposure. These headwinds are real, but they are manageable for a company with a close to $100 billion market capitalization, a well-covered payout ratio of 39%, and a history of navigating operating complexity with discipline.

This stock has been added with an increased position in the Dividend Protection Stocks Portfolio, reflecting a conviction that its combination of low market correlation, fortress-like dividend track record, and long-dated contracted revenue streams aligns precisely with the portfolio’s mandate of capital preservation and reliable income for risk-averse investors.