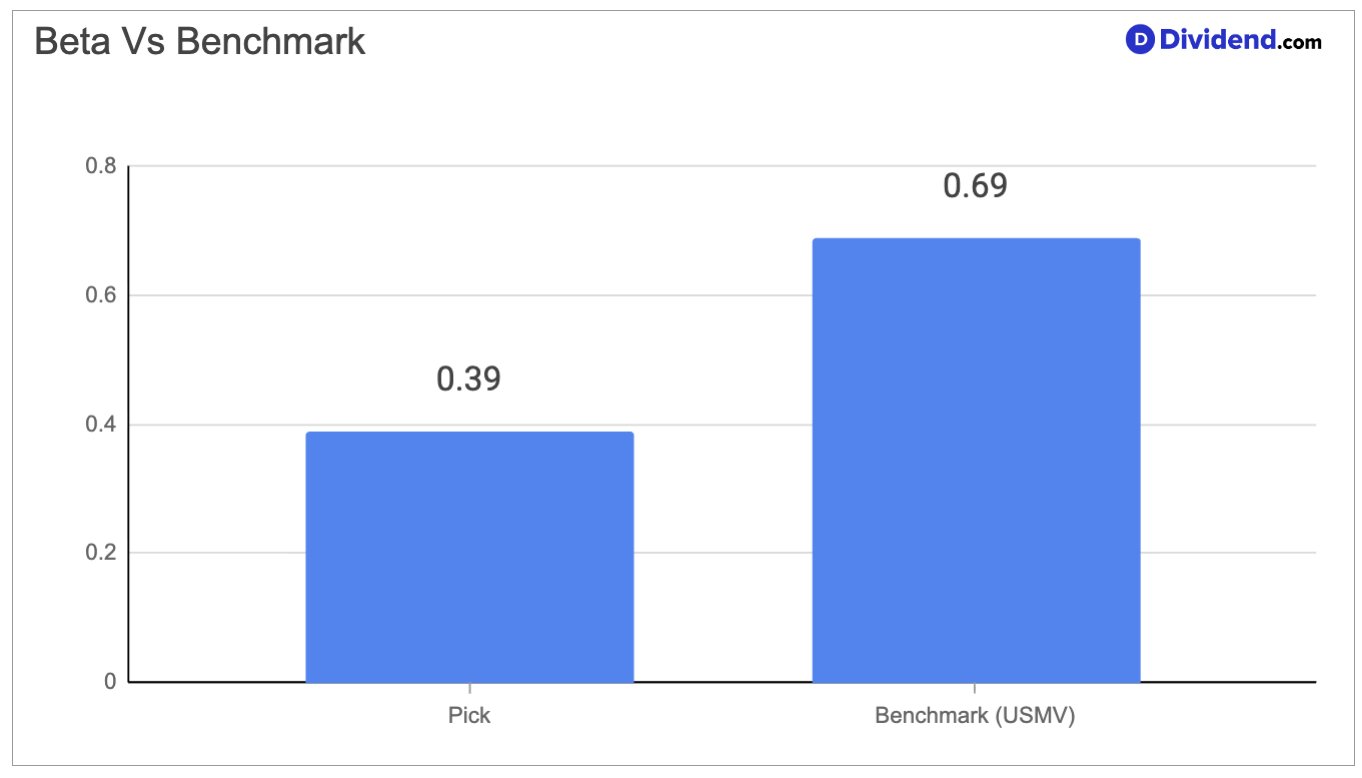

This biopharmaceutical company operates in the health care sector, focusing on developing medicines for serious illnesses in virology, oncology, and inflammation areas. Its core business includes treatments for HIV and hepatitis, along with cell therapies and targeted cancer drugs. The firm benefits from strong demand in HIV prevention and treatment, where a new long-acting injectable has driven significant growth. Revenue streams are stable due to established products with high efficacy and global reach. However, policy changes in drug pricing and competition in oncology present challenges. With a low beta of 0.39, the stock shows limited volatility, making it suitable for risk-averse investors. Cash flows remain robust, supported by high margins and a long patent runway.

The company’s growth comes from expanding its HIV portfolio, including prevention options that simplify patient regimens and increase access. In oncology, acquisitions have added innovative therapies, though sales in some areas face competitive pressures. Risks include regulatory headwinds from government policies that shift costs to manufacturers, impacting profitability. Despite these, the firm maintains a solid balance sheet with manageable debt, enabling continued investment in research.

We added this stock to our Dividend Protection Stocks Portfolio because its defensive cash flows from essential medicines align with the mandate for safe, reliable income. This action reflects confidence in its ability to deliver consistent dividends amid market uncertainties. Investors can expect stability from its proven track record in payout growth.