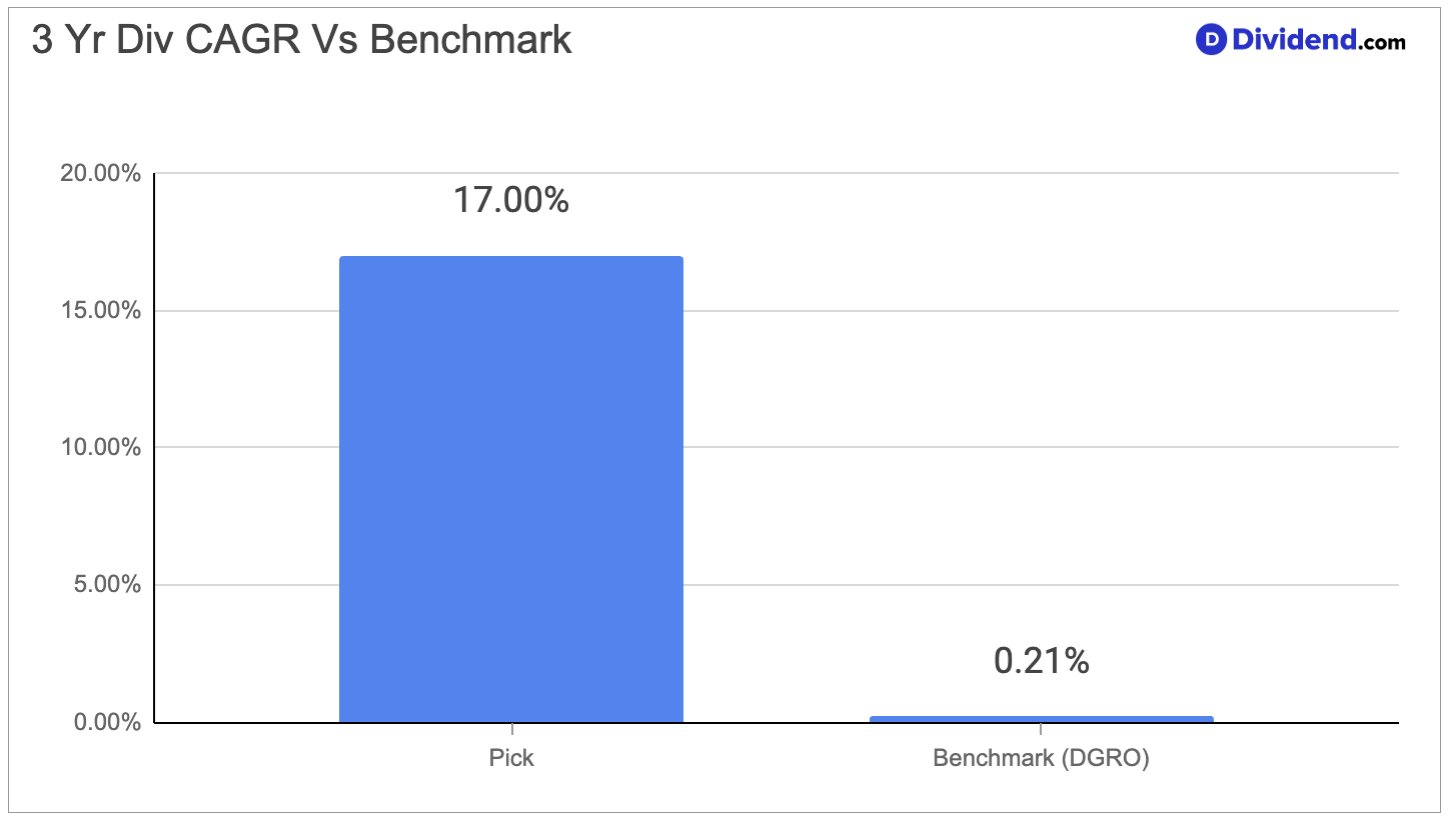

A regional bank anchored in a recovering island economy is doing something that most financial institutions its size are not: growing its dividend at 17% annually over the past 3 years, a pace that places it firmly in the top 20% of all dividend stocks tracked by Dividend.com. That growth is not a one-off event driven by a bounce from an artificially low base — it reflects a deliberate, multi-year capital return strategy supported by expanding loan volumes, technology-driven cost discipline, and a consumer banking franchise that is deepening its market share across retail, small business, and mass-affluent customer segments. For dividend growth investors, a 17% 3-year dividend CAGR is precisely the kind of compounding signal that the portfolio is designed to capture.

The business behind this dividend story is the second-largest locally chartered bank in its home market, operating across retail banking, commercial lending, and wealth management and insurance. Its product suite covers deposit accounts, auto and consumer loans, residential mortgages, commercial real estate financing, and investment distribution — a full-service banking model designed to serve households and businesses at every stage of financial life. Growth is being driven by a multi-year digital transformation that has increased retail enrollment, deepened cross-sell penetration within its targeted customer segments, and kept expense growth flat even as the loan book expands. The local economy where it operates is in a sustained recovery phase, supported by federal reconstruction funding, low unemployment, and strong consumer liquidity, all of which are feeding loan demand and deposit generation.

The principal risk on the horizon is sensitivity to interest rate movements, since earnings guidance for the rest of 2026 assumes the Federal Reserve holds rates steady — a reasonable assumption today, but one that introduces earnings variability if monetary policy pivots. Energy and fuel cost inflation, given the geographic isolation of the market, is a secondary operational risk that management monitors closely.

Increasing our position in the Dividend Growth Stocks Portfolio reflects confidence that this bank’s dividend growth trajectory is durable, that its capital return discipline is backed by genuine earnings quality, and that its overall score of 4.10 out of 5 — with a Buy signal and a rank of 8th among the 12 current Buy-rated names — reflects a high-conviction, well-rounded opportunity for investors who prioritize compounding income growth.