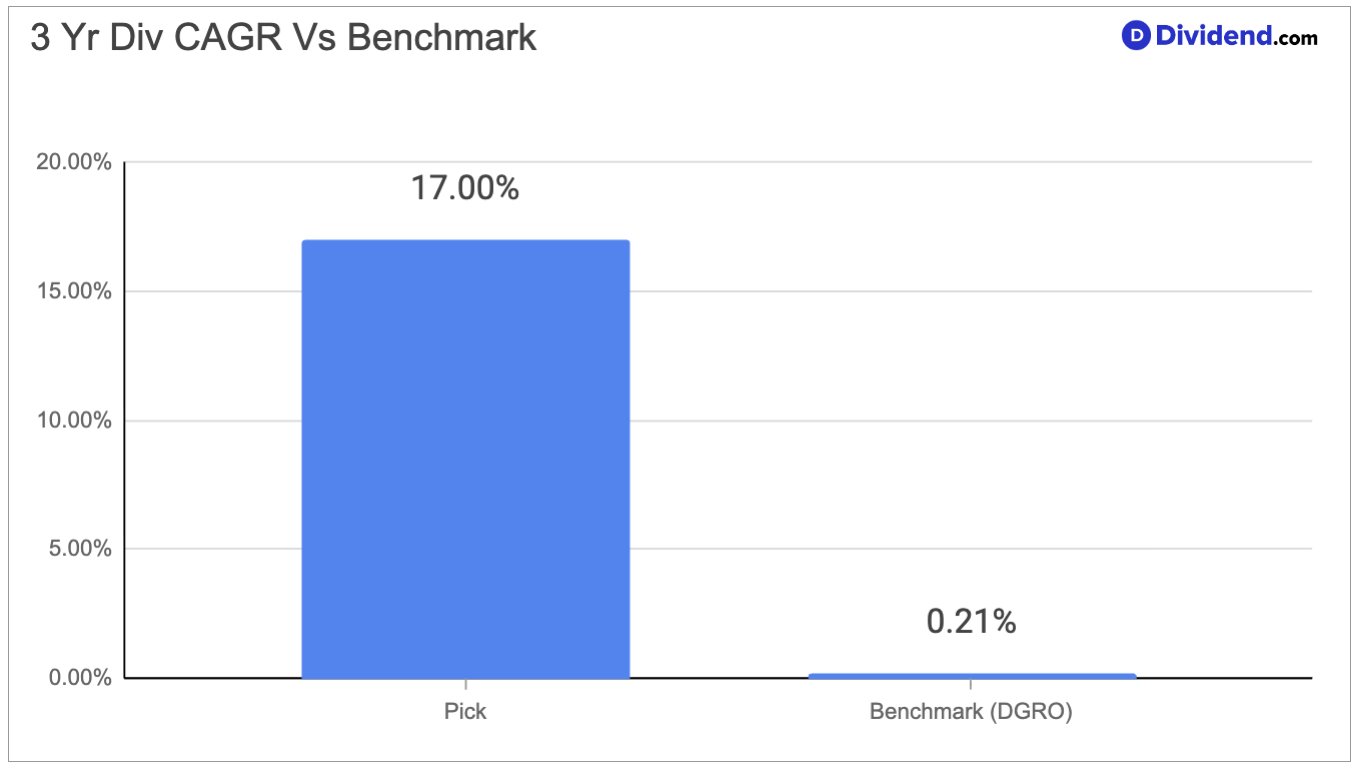

Peru’s dominant financial holding company — operating across universal banking, microfinance, insurance, pensions, and investment management — has delivered a 17% 3-year dividend CAGR, placing it firmly in the top 20% of all dividend stocks globally. That growth rate is more than three times the banking sector average of 5%, making this an unusually compelling story for investors who prioritize dividend compounding over raw yield. The group’s flagship banking subsidiary commands roughly 36% market share in its home country, nearly double its closest competitor, and that scale advantage underpins the low-cost deposit base that supports both profitability and growing shareholder payouts.

The company’s business model spans traditional lending, micro-entrepreneur financing, health insurance, pension management, and capital markets services — a diversified financial ecosystem that reduces dependence on any single revenue stream. A particularly powerful element of the current growth narrative is the group’s mobile payments and micro-lending app, which reached profitability in 2024 and now serves approximately 15.5 million monthly active users, representing a substantial share of the country’s economically active population. This digital platform is rapidly evolving from a payments utility into a full-fledged lending business, with management expecting the app’s loan book to roughly triple over the next two years. The combination of a dominant traditional banking franchise and a fast-scaling digital business creates a dual-engine growth profile that supports both near-term earnings momentum and long-term dividend expansion.

Risks do exist and should not be overlooked. The company’s regional exposure includes operations in Bolivia, where currency devaluation is expected to shave approximately 1 percentage point off consolidated loan growth in 2026. Ongoing pension fund withdrawals in the domestic market may also moderate long-term activity in the retirement savings segment. Additionally, the rapid expansion of unsecured digital lending introduces a layer of credit quality uncertainty as the portfolio matures. These factors are manageable within the context of a well-capitalized, highly profitable institution, but they are relevant inputs for any dividend growth investor assessing durability across economic cycles.

This stock has been reaffirmed in the Dividend Growth Stocks Portfolio, reflecting its continued alignment with the portfolio’s mandate of identifying companies with demonstrated dividend growth momentum, sound financial discipline, and a credible pathway for sustained payout increases over the long term.