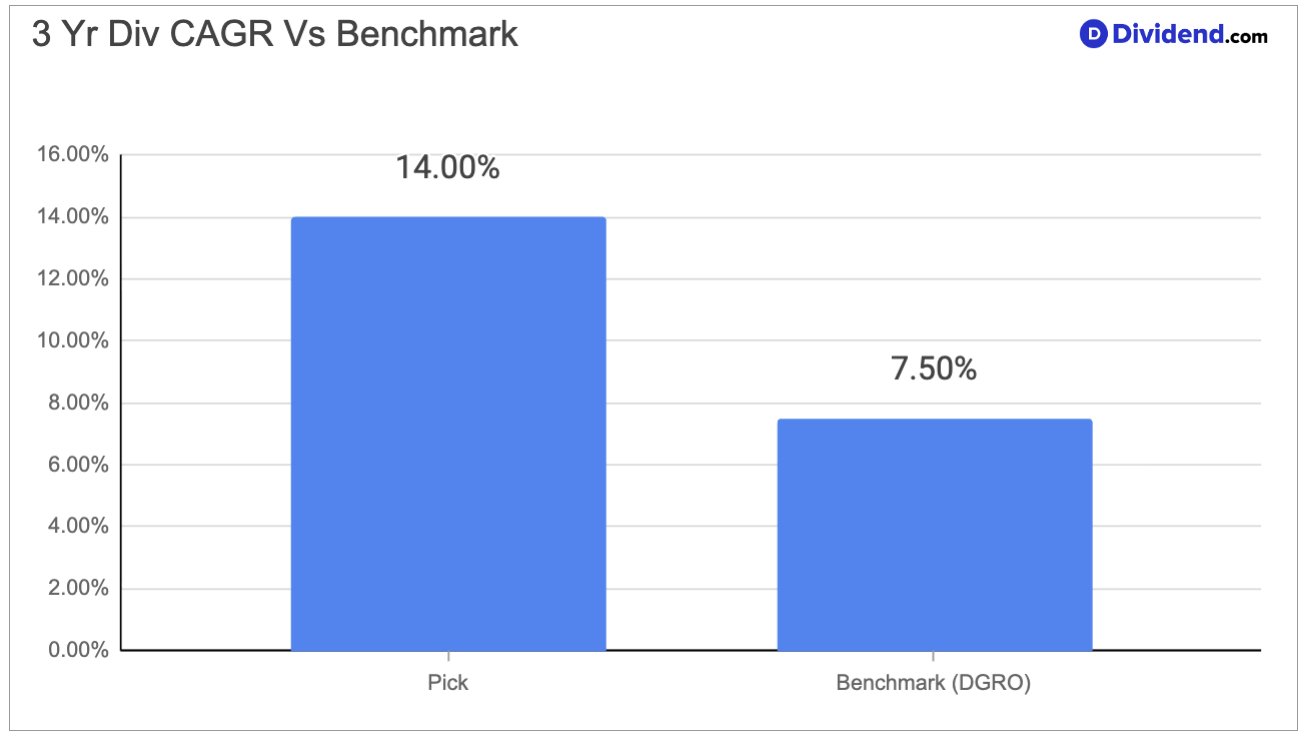

This diversified financial services firm stands out with its 14% 3-year dividend CAGR, reflecting strong growth in consumer banking, investment banking, and asset management. The company benefits from resilient consumer trends, record inflows in wealth management, and strategic investments in technology and partnerships that enhance its payments and card ecosystems. However, it faces regulatory pressures on credit card rates, integration challenges from new acquisitions, and competitive deposit dynamics from fintech rivals.

Operating in a dynamic environment, the firm reported solid Q4 2025 results, including 7% revenue growth to over $45 billion, driven by markets revenue and asset fees. Net income reached $13 billion, with EPS at $4.63, despite a reserve build for a card portfolio commitment. Full-year adjusted net income crossed the $55 billion mark, showcasing execution amid uncertainties. Growth drivers include adding millions of new accounts in checking and cards, plus $500+ billion in annual client asset inflows. Risks involve geopolitical tensions, fiscal deficits, and potential credit availability reductions from rate caps, yet managed exposures and optimistic deal pipelines position it well for 2026.

We increased our position in the Dividend Growth Stocks Portfolio because this stock aligns with our focus on consistent dividend growers that offer long-term capital appreciation. Its durable earnings from diverse segments support ongoing increases, fitting our mandate for market outperformance through compounded growth. This move strengthens our exposure to a resilient player in global finance.