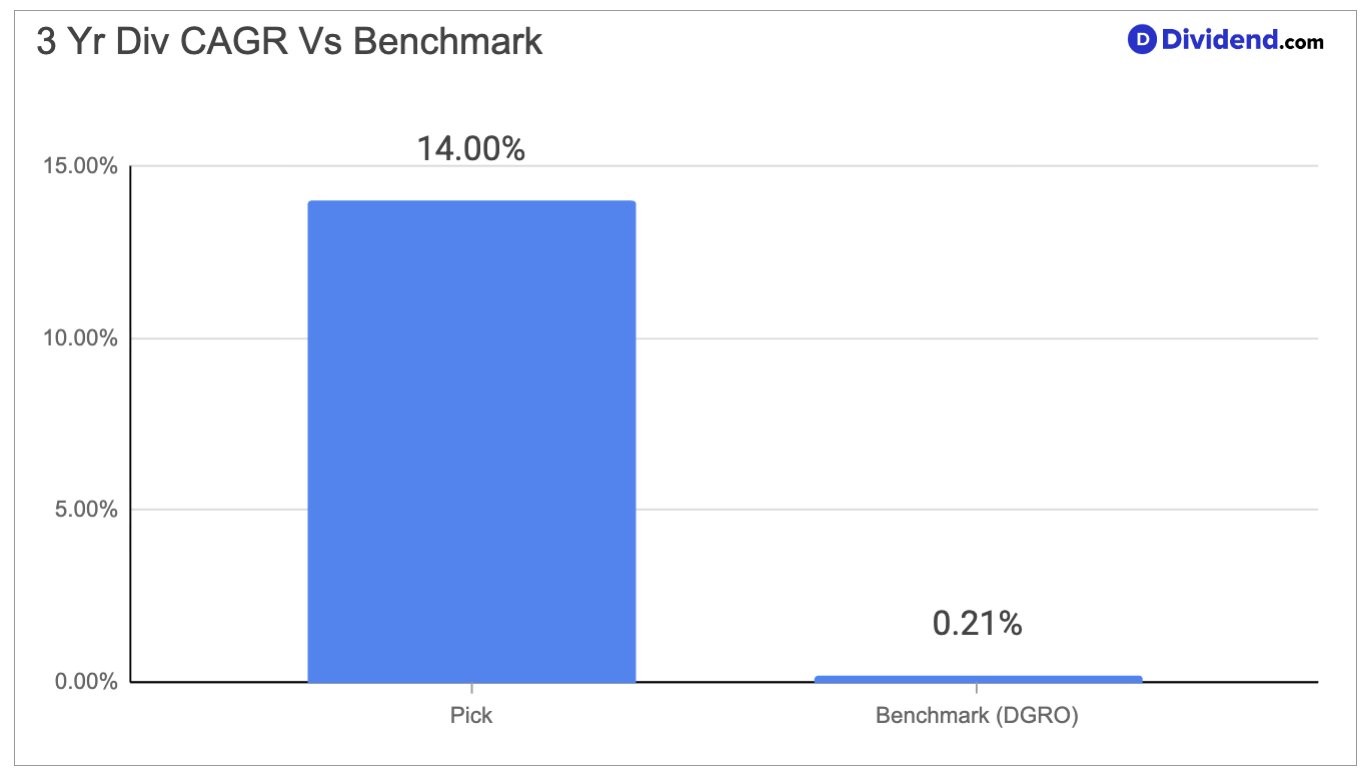

Few financial institutions combine scale, consistency, and dividend momentum the way this global banking leader does. Operating across retail deposits, credit cards, investment banking, capital markets, and wealth management, the firm is not merely large — it is deeply embedded in how households, businesses, and governments move and manage money. Its 14% 3-year dividend CAGR ranks in the top 20% of all dividend stocks, a figure that reflects not just growth ambition but the earnings durability required to sustain such increases over time.

The business has grown its revenue base by expanding across multiple client segments and geographies, with recent strength coming from market activity, asset management fee growth, and franchise expansion, including 1.7 million net new checking accounts in a single quarter. These growth drivers are not dependent on one product or region, which makes the compounding dividend story more credible. The firm does face meaningful headwinds, including regulatory exposure around consumer lending rate policies, elevated risk-weighted assets from an ongoing credit card portfolio integration, and competitive deposit pressures from fintechs. These are risks that warrant attention, but they do not appear structurally disqualifying given the firm’s capital strength and through-cycle track record.

This combination of broad-based revenue growth, disciplined capital return, and a decade-and-a-half of uninterrupted dividend increases made a compelling case for increasing the position in the Dividend Growth Stocks Portfolio — a portfolio built on the conviction that consistent dividend growers, compounded over time, can deliver meaningful outperformance.