For decades, investors have framed portfolio construction as a binary choice: active or passive. On one side sits passive investing, offering low-cost, broad market exposure and predictable outcomes. On the other hand, sits active management, promising the potential for outperformance through research, security selection, and tactical positioning.

In reality, most investors today land somewhere in the middle.

The idea is simple but powerful: by adding a small amount of active decision-making to a passive foundation, investors can potentially improve returns, manage risk more effectively, and achieve more consistent outcomes—all without significantly increasing costs or volatility. Rather than treating active ETFs as peripheral additions, investors are increasingly using them within the core itself, in what is known as enhanced indexing.

The Limits of Pure Passive and Pure Active

When building a portfolio, investors essentially face two basic choices: go passive and index, or choose an active manager.

Passive investing has grown tremendously for good reason, offering low fees, transparency, and broad market exposure. However, passive strategies carry a key limitation: they guarantee market returns—nothing more, nothing less.

That fact becomes particularly important in today’s environment. Markets are increasingly concentrated, with a handful of mega-cap stocks driving a large share of index returns, creating hidden risks as passive investors may unknowingly become overexposed to specific sectors or companies.

At the same time, active management on its own can be inconsistent. While some managers outperform, many underperform after fees, making it difficult for investors to identify winners in advance.

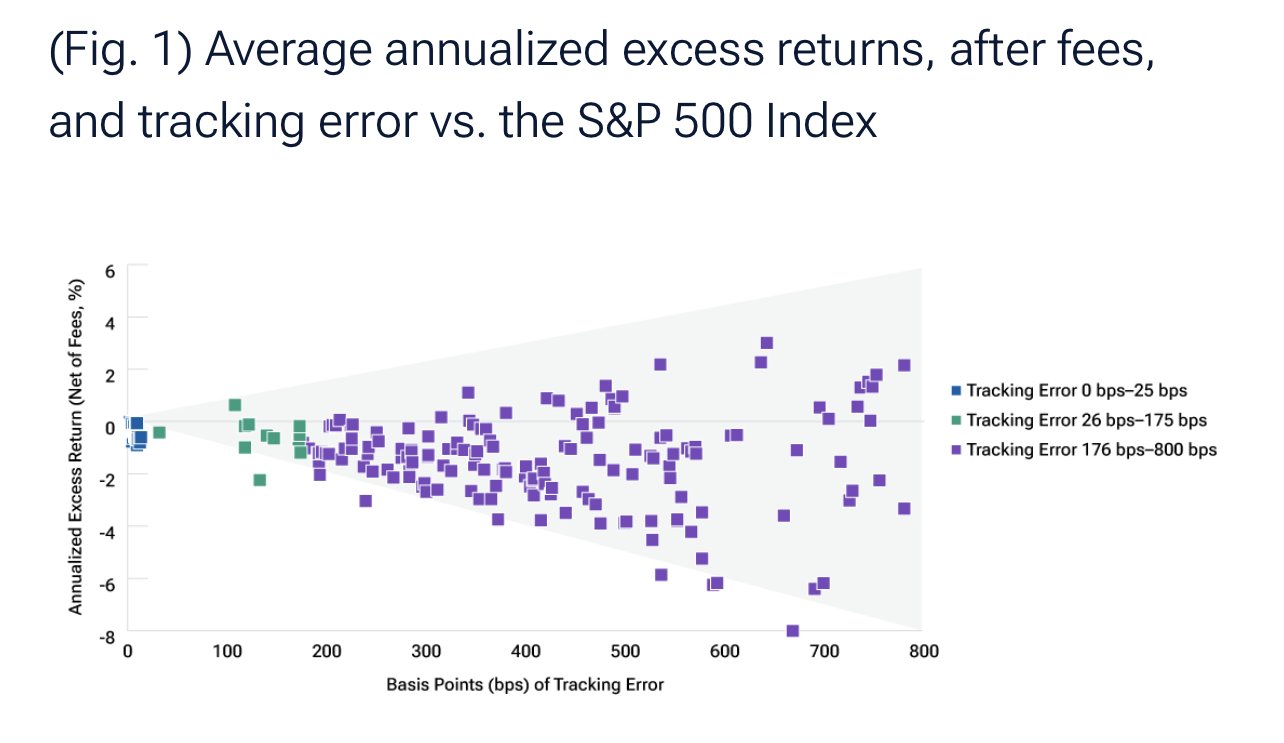

This dynamic is visible in the growing dispersion of returns within large-cap equity markets.

While headline index performance may appear steady, the reality beneath the surface is far more uneven. Different stocks—even within the same sector—can experience vastly different outcomes based on earnings growth, balance sheet strength, competitive positioning, and macro sensitivity.

According to T. Rowe, this dispersion can be a problem. Funds with higher tracking error can outperform, but the dispersion in results does not produce smooth returns, making manager selection critical.

Analysts at T. Rowe Price highlight this fact in the following graph.

Source: T. Rowe Price

The Case for Blending Approaches

The question for investors is what to do, since both strategies offer portfolio wins but also carry significant pitfalls.

For some investors, blending the two into a core-and-satellite approach has been the answer, but that approach is not perfect and does not fully eliminate their respective issues. Selecting the wrong manager at the wrong time can reduce the effectiveness of a passive core, and return volatility can hinder a portfolio. Moreover, for some investors—especially endowments, pension funds, and other institutions—adding active strategies may exceed their risk budgets.

So how can investors boost their core portfolios, gain the potential for outperformance, and remain benchmark-aware? The answer may lie in fundamental or enhanced indexing.

Enhanced active strategies—also known as enhanced indexing, fundamental indexing, or systematic equity—aim to combine the best of active and passive strategies in one package. Managers take an index and apply small active adjustments to the benchmark, such as value screens, balance sheet analysis, or momentum and dividend-yield scoring, using these systematic elements to tweak the index’s holdings.

The goal is to deliver steady, index-like beta with a consistent extra boost to performance while remaining benchmark aware. It is the focus on consistency of positive performance rather than magnitude that makes enhanced active strategies work—just a few tenths of a basis point, year in and year out.

Those extra basis points make a real difference when compounded consistently over time. According to T. Rowe Price, a slight 0.50 basis point increase to annual returns can result in an additional five years of retirement spending. 1

Enhanced indexing allows managers to achieve these slight performance bumps by not swinging for the fences and instead getting consistent base hits.

How to Implement Enhanced Indexing in a Portfolio

These enhanced indexing strategies work well in active ETFs. Thanks to lower costs, the active ETF structure allows managers to clear lower fee hurdles, which can deliver the consistent few extra basis points needed for enhanced returns. For investors, this means boosting their core portfolio while keeping risks lower and generating additional returns.

For many investors, replacing a broader index fund with an enhanced ETF—or using the enhanced fund as a satellite position—can help generate the added returns needed to improve their outcomes.

Enhanced Active ETFs

These ETFs provide exposure to enhanced or fundamental strategies with an active touch, with expense ratios between 0.17% and 0.28% and assets under management between $3.3B and $21B. They are sorted by their YTD total return, which ranges from -0.4% to 6.2%. They are currently yielding between 0.46% and 1.5%.

| Ticker | Name | AUM | YTD Total Ret (%) | Yield (%) | Exp Ratio | Security Type | Actively Managed? |

|---|---|---|---|---|---|---|---|

| DFUV | Dimensional U.S. Marketwide Value ETF | $8.5B | 6.2% | 1.5% | 0.21% | ETF | Yes |

| DFAC | Dimensional U.S. Core Equity 2 ETF | $20.9B | 5.7% | 0.8% | 0.17% | ETF | Yes |

| FELC | Fidelity Enhanced Large Cap Core ETF | $4.5B | 3.3% | 1.04% | 0.19% | ETF | Yes |

| FELG | Fidelity Enhanced Large Cap Growth ETF | $3.3B | 2.4% | 0.46% | 0.19% | ETF | Yes |

| AVUV | Avantis U.S. Small-Cap Value ETF | $6.7B | 0.80% | 1.4% | 0.25% | ETF | Yes |

| DFAT | Dimensional U.S. Targeted Value ETF | $8.2B | -0.4% | 0.8% | 0.28% | ETF | Yes |

The case for blending active and passive strategies is particularly strong in today’s market environment. Markets are more complex, concentrated, and dynamic than ever, meaning passive investing alone can expose portfolios to unintended risks, while fully active approaches may introduce inconsistency. Enhanced indexing offers a balanced solution.

Bottom Line

The debate between active and passive investing is increasingly outdated. Today’s most effective portfolios are built not on choosing one approach over the other, but on integrating both, and enhanced indexing is the solution that meets that need.

1 T.Rowe Price (February 2026). Smarter alpha: Get more from a portfolio’s core